The Power of Logistics to Move the World!

It's the Power of extrans.

EXTRANS GLOBAL - Air Freight News - Week 17 2026

Air Cargo Market Highlights

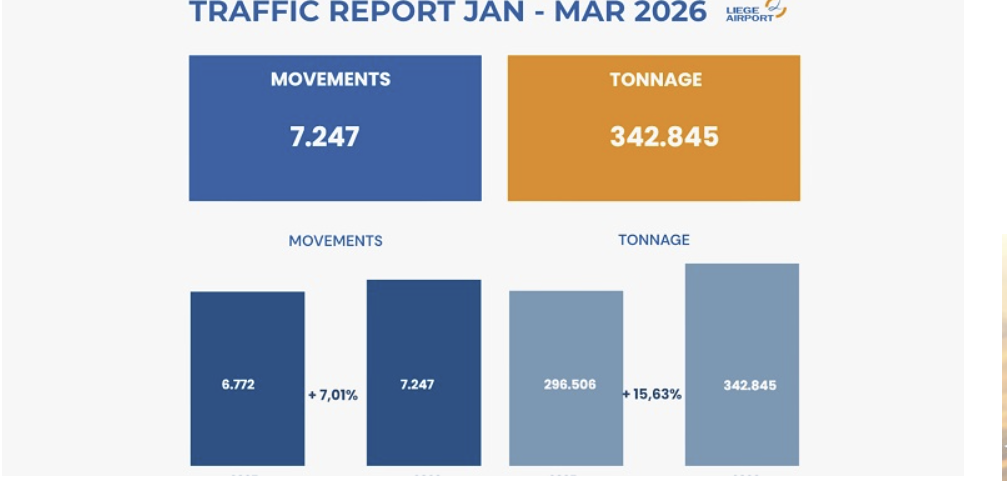

1) Liège Airport Q1 Cargo Up 16% – E‑Commerce Drives Demand Growth

Belgium’s Liège Airport posted solid results in the first quarter of 2026, sustaining its air cargo growth momentum from last year.

From January to March 2026, aircraft movements rose 7% year‑on‑year, while cargo throughput expanded by 16%.

In March alone, flight frequencies increased 9% and cargo volumes climbed 11%, reflecting a steady upward trend.

Outbound cargo also maintained strong growth, with export volumes surging 20% year‑on‑year in 2026.

This further consolidates Liège Airport’s competitiveness in the global air cargo network, driven by robust e‑commerce expansion and rising international logistics flows.

Laurent Jossart, CEO of Liège Airport, stated that the airport is taking a prudent approach amid current market conditions.

“The overall outlook remains positive, yet 2026 will continue to bring rapid market shifts and high operational pressures,” he commented, adding that the airport remains reasonably confident in long‑term growth while closely monitoring market developments for the remainder of the year.

2) Korean Air Vice Chairman Woo Ki‑hong: Fleet to Expand Sharply to 270 Aircraft

Following its merger with Asiana Airlines, Korean Air unveiled aggressive expansion plans, including new routes to Europe, India and other regions.

Once integrated into a global mega‑carrier, the airline aims to further scale its operations to compete with leading international carriers.

In a written interview with a German media outlet on the 15th, Vice Chairman Woo Ki‑hong announced that Korean Air’s combined passenger and cargo fleet, currently totaling 230 aircraft including Asiana, will expand to 270 units by 2037.

The expansion will focus on modernization, replacing ageing aircraft with next‑generation, fuel‑efficient models rather than simple quantity growth.

He emphasized that evolving into a mega‑carrier through integration is not a choice but an essential requirement for survival.

“Combining capabilities to achieve economies of scale and operational efficiency is the only way to compete on equal footing with major global airlines,” he explained.

The fully integrated new Korean Air is scheduled to officially launch on December 17 this year.

3) Freightos: Hormuz Disruption Continues to Fuel Rate Hikes – Sea & Air Freight Costs Rise in Tandem

Global Logistics Faces Widespread Fuel Risk

According to Freightos’ weekly briefing, escalating tensions in the Middle East and the ongoing blockade of the Strait of Hormuz are sending ripple effects across global supply chains, pushing both ocean and air freight rates higher.

Prolonged fuel supply disruptions risk triggering permanent structural cost inflation across all logistics sectors.

Air Cargo Hit by Fuel Shock – Falling Capacity & Rising Rates Occur Simultaneously

The Middle East supplies roughly 20% of the world’s jet fuel.

Since the strait closure, jet fuel prices have more than doubled, prompting major airlines to reduce operations:

- Vietnam Airlines: Approx. 20% flight cutbacks

- Cathay Pacific: 2% capacity reduction starting mid‑May

- Delta Air Lines, United Airlines: Downsizing low‑profit routes

China’s suspension of jet fuel exports has further tightened supply across Asia.

Many foreign carriers now refuel in third countries en route to mitigate shortages.

Middle Eastern flight frequencies are estimated to have dropped by around 60% compared to pre‑conflict levels.

Gulf carriers rely heavily on passenger bellyhold capacity for cargo transport; prolonged weakness in passenger travel will therefore delay any meaningful recovery in air cargo supply.

Rate pressure remains firm across key trade lanes:

- South Asia – Europe: $5.15/kg (2 times pre‑conflict levels)

- Southeast Asia – Europe: $5.30/kg (+60%)

- China – North America: $6.30/kg (stable, down from a late‑March peak of $7.50/kg)

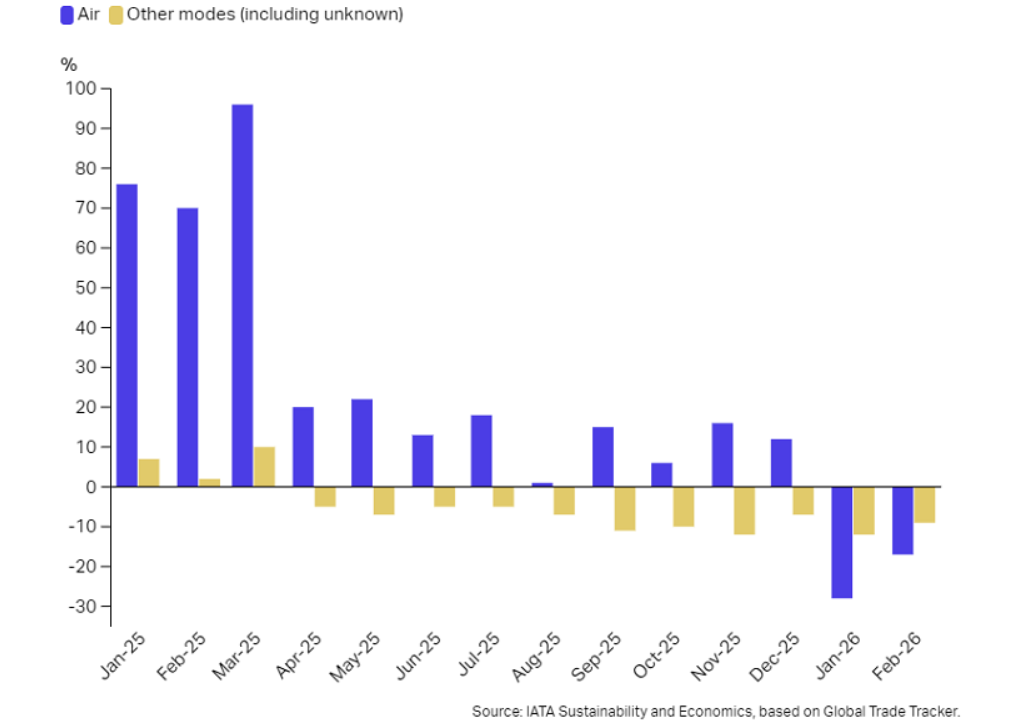

4) IATA: Air Cargo Acts as Critical US Import Shock Absorber, Remains Indispensable Amid Tariff Uncertainty

After enabling large‑scale frontloading for U.S. importers in early 2025, air cargo continues to fulfill a vital strategic role throughout 2026, with IATA highlighting its growing importance compared to other transport modes.

IATA’s weekly analysis shows that U.S. import volumes surged sharply in Q1 2025 as businesses rushed to stock up ahead of anticipated tariff increases.

Air cargo served as the critical backbone supporting this massive frontloading trend.

Cargo value transported by air jumped 70%–95% year‑on‑year in the first three months of 2025, while growth in sea and other transport modes remained limited.

Over 80% of all incremental import volumes during this period were moved by air freight.

Air cargo’s unmatched speed and flexibility have reinforced its strategic value as a global trade shock absorber, a function previously proven during the COVID‑19 pandemic.

Market dynamics shifted from Q2 2025 onward.

With new tariffs fully implemented, frontloading demand faded, slowing the growth of air imports.

One year after the enforcement of the so‑called “Liberation Day” trade policies, the abnormal surge in early‑2025 inventory stocking has subsided.

Even so, air cargo retains strong strategic importance.

Driven by rising demand for high‑value and urgent shipments such as AI equipment, alongside persistent trade policy uncertainty, air freight has solidified its position as a premium import solution for the United States.

Share this article :

top