The Power of Logistics to Move the World!

It's the Power of extrans.

EXTRANS GLOBAL - Air Freight News - Week 16 2026

Air Cargo Market Update

1) US-Iran 2-Week Ceasefire – Jet Fuel Supply & Prices to Take Months to Normalize

Despite a two‑week ceasefire agreement between the US and Iran amid severe jet fuel supply disruptions caused by the Iran conflict, the aviation industry forecasts that jet fuel supply and price normalization will still take months.

Willie Walsh, Director General of the International Air Transport Association (IATA), made the statement to reporters at an event in Singapore.

“Given disruptions to petroleum refining capacity in the Middle East, it will still take months to recover to necessary supply levels. It is unlikely to recover within a matter of weeks,” he noted.

He added that even though crude prices fell 16% following the ceasefire, “people may expect jet fuel to drop by a similar margin, but prices will remain elevated,” which “will lead to higher airfares. It is inevitable.”

Following US President Donald Trump’s announcement of the two‑week truce, May WTI crude futures plunged more than 19% intraday to $91.05 per barrel.

Near‑term risks of jet fuel shortages persist, with Asia the most vulnerable region, followed by Africa and Europe.

However, Walsh also pointed out that “refining margins are currently high, giving refiners incentive to increase jet fuel production.”

He expects South Korean and Chinese refiners to resume exports of refined products including jet fuel once crude supply resumes.

Since the outbreak of the Iran conflict in late February, jet fuel prices have more than doubled, with widespread supply shortages.

Airlines worldwide have been operating in emergency mode by raising fares and cutting flights.

Especially hard‑hit are airlines in low‑income, highly jet‑fuel‑dependent countries such as Vietnam, Myanmar, and Pakistan, due to suspended or reduced jet fuel exports from refiners in China, Thailand, and South Korea.

2) Main Driver of Air Cargo Rate Hikes Shifts – From Capacity Shortages to Fuel Cost Shock

![]()

According to WorldACD data, the global average air cargo rate has surged to $3.10/kg – up 20% year‑on‑year and 11% from two weeks ago.

In Week 14 of this year (March 30 – April 5), rates spiked sharply even as both supply and demand softened across the global air cargo market.

- Middle East & Southeast Asia rates soared 64% YoY

- Europe and Africa origin rates rose 28% and 25% YoY

- North America +17%, Asia Pacific +12%

Demand by chargeable weight fell 2% YoY overall, led by Middle East & Southeast Asia (-7%), Europe (-5%), and Africa (-9%).

Central & South America rose 1%, while Asia Pacific remained flat.

Global capacity also decreased 4% YoY, with Middle East & Southeast Asia plunging 29% – the sharpest drop.

Africa capacity fell 4%, while Asia Pacific, Europe, and Central & South America each expanded 1%.

Compared with two weeks prior:

- Asia Pacific → North America: demand +2%, rates +12%

- Intra‑Asia: demand -2%, rates +8%

- Asia → Europe: demand +2% by chargeable weight, rates +1%

3) Air Premia Out of Turbulence but Facing Diminishing Cash Generation

Air Premia’s immediate challenge is survival, not expansion.

Mounting debt burdens and declining cash generation are putting its long‑term financial strategy to the test.

Its EBITDA‑to‑financial expense ratio fell from 1.9x in 2024 to just 0.8x last year, meaning it could not cover interest payments even by using all operating profit.

Saddled with excessive debt, Air Premia’s key tasks are managing debt obligations and liquidity for planned additional fleet investments.

Total borrowings reached KRW 1.0505 trillion at the end of last year, with short‑term debt maturing within one year rising to 8.07%.

Financial expenses nearly doubled from KRW 47.1 billion in 2024 to KRW 70 billion last year, up roughly 50%.

The financial expense ratio rose from 9.58% in 2024 to 11.79% last year.

Revenue grew 20.75% over the period, while financial expenses surged 48.62%.

Following an operating loss, a sharp rise in non‑operating expenses pushed the net loss to a record high of KRW 75.5 billion last year (operating loss KRW 31.9 billion + non‑operating loss KRW 53.9 billion), driven largely by financial costs.

The company’s financial position is unlikely to improve in the short term, raising risks of a vicious cycle of rising lease burdens and further weakening cash generation.

Against a backdrop of high exchange rates and soaring fuel prices, Air Premia’s long‑haul route expansion strategy is expected to become a liability.

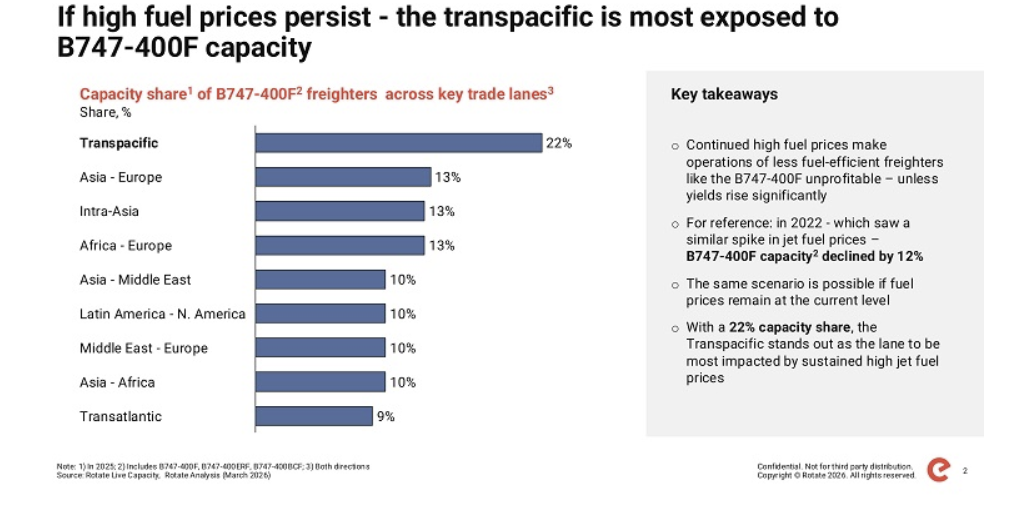

4) B747F Hits Profitability Limit Amid Fuel Surge – Carriers Consider Fleet Restructuring

Sky‑high fuel prices originating from the Middle East are squeezing air cargo profitability, with particularly steep declines for fuel‑inefficient B747 freighters.

Structural changes to airlines’ fleet strategies appear inevitable.

Although higher yields and various surcharges have partially offset cost increases, profitability gaps between aircraft types are widening rapidly.

Jet fuel prices peaked in March at $4.45 per gallon, drastically increasing fuel costs for airlines.

Under identical conditions, performance varies sharply: the B777F remains solidly profitable at current rate levels.

By contrast, B747 freighters (B747F and B747‑400F) are now near break‑even or already negative on some routes.

Especially on lanes with limited rate upside, higher fuel costs cannot be absorbed, pushing these aircraft firmly into loss‑making territory.

“While rate increases and surcharges have softened some fuel cost pressure, fuel‑intensive aircraft have reached their profitability limit,” analysts noted.

Beyond short‑term cost pressure, this trend could reshape long‑term supply dynamics.

The B747‑400F series still accounts for a substantial share of global freighter capacity, notably around 22% on trans‑Pacific lanes.

Share this article :

top