The Power of Logistics to Move the World!

It's the Power of extrans.

EXTRANS GLOBAL - Air Freight News - Week 15 2026

Air Cargo Market Update

1) Severe Capacity Collapse at Middle Eastern Hub Airports – Doha Down 77% YoY

The aftermath of the Middle East conflict is rapidly reshaping the global air cargo supply structure. Capacity at major Middle Eastern hubs has shrunk dramatically, causing structural shifts across the air cargo market.

Based on data from March 24–30, 2026, many of the world’s top 10 airports by air cargo capacity change are located in the Middle East. This indicates the impact extends beyond regional disruption and is shaking the core pillars of the global air cargo network.

The sharpest decline was recorded in Doha, Qatar, with capacity down by roughly 37,000 tonnes, representing a 77% year-on-year collapse.

Major Gulf hubs including Dubai (DXB), Al Maktoum (DWC), Bahrain (BAH), and Kuwait (KWI) also saw capacity plummet by 50% to 100%, suffering near‑network‑paralysis levels of disruption.

Some airports effectively halted operations entirely (-99% to -100%) – an extraordinary outcome given the region’s strategic role in global air cargo flows.

These supply shifts are not only disrupting cargo flows but directly driving up rates and triggering structural changes in demand.

So far, shippers have accepted high rates to maintain supply chain stability and service reliability. However, prolonged jet fuel inflation and global economic uncertainty could significantly weaken demand.

Routes highly dependent on Middle Eastern transit – especially Asia–Europe and South Asia–Americas – face growing rate volatility and operational uncertainty.

2) Main Driver of Air Cargo Rate Hikes Shifts – From Capacity Shortages to Fuel Cost Shock

As the global air cargo market’s recovery slows, the primary force behind rising rates is quickly shifting from capacity constraints to soaring fuel costs.

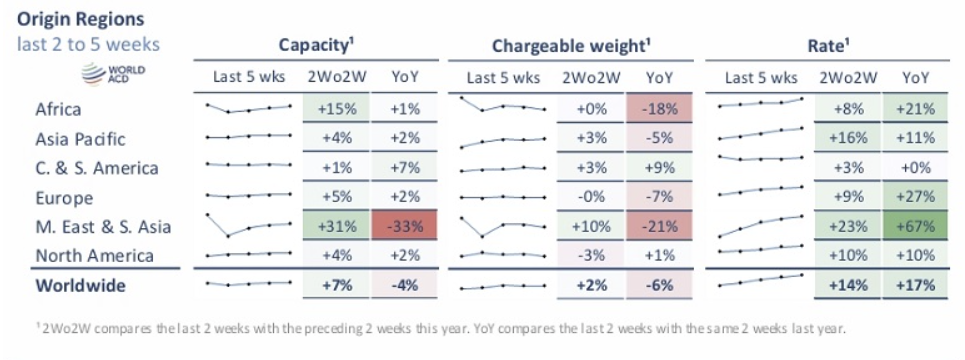

According to WorldACD data, during March 23–29 (Week 13), global air cargo volumes were flat week-on-week. Some regions declined, others saw modest growth, reflecting overall weak demand recovery.

Meanwhile, the global average air cargo rate hit a year-to-date high of $2.98 per kg, although the pace of increase slowed from +10% in Week 11 to +5% recently. Jet fuel prices have more than doubled since the Iran conflict began in late February, reaching record levels in March.

“Capacity growth outpaces demand” – Global volumes decline

- Demand clearly lags capacity expansion. Only Asia Pacific (+2%) and Europe (+1%) posted mild growth.

- Middle East & South Asia, Africa, and North America all fell -4%; Latin America -1%.

- Global volumes were -6% YoY, with most regions contracting except Latin America (+7%). MESA (-25%) and Africa (-21%) led the decline.

- Americas routes also weakened sharply: Dubai (-44%), Bangladesh (-40%) plunged, while India was a rare exception at +6%.

Asia-origin rates surge – double-digit gains in Korea and China

- Asia Pacific–Americas rates rose +9% WoW to $5.91/kg.

- Korea and China each jumped +13%, followed by Hong Kong (+12%) and Singapore (+10%).

- Asia–Europe rates also strengthened: +4% WoW, +28% YoY.

- Indonesia-origin rates surged +41% WoW (+115% YoY); Taiwan and Singapore +9% WoW, but volumes remained stagnant.

- Americas route volumes were flat; Europe routes up only +1%, confirming rate hikes are cost-driven, not demand-led.

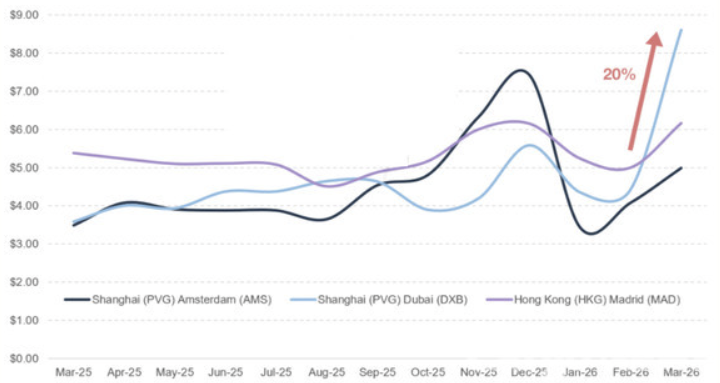

3) Iran Conflict Pushes Air Cargo Rates Up 95%

The Iran conflict caused air cargo rates in March to surge 95% compared to February.

- Shanghai (PVG)–Dubai (DXB) reached **$8.60/kg** (up 95%). With fuel surcharges, it hit $9.40/kg, exceeding pandemic-era levels.

- Singapore (SIN)–London (LHR) saw fuel surcharges jump nearly 290%, with security surcharges also soaring.

- Security surcharges on Dubai (DXB) & Abu Dhabi (AUH)–Amsterdam (AMS) rose 44%.

- Mumbai (BOM) & Delhi (DEL)–Madrid (MAD) all-in rates rose 27% in March, with fuel surcharges up 21%.

Top‑20 global cargo carriers including Qatar Airways (QR), Emirates (EK), and Etihad (EY) are operating reduced schedules.

Around 15.6% of global air cargo transits via the Middle East, and Gulf airlines account for 18.2% of global air cargo capacity. The resulting bottlenecks are severely disrupting the air cargo market.

Over half of all international air cargo routes saw rates rise by more than 20% in March.

4) Fuel Surcharges Triple – Expected to Rise Further in May

Fuel surcharges on airline tickets have already jumped more than threefold due to the Middle East war, with May surcharges projected to hit all-time highs.

This risks depressing passenger demand, widening carrier losses and increasing earnings pressure.

The Singapore jet fuel average (MOPS) for the current surcharge period (Feb 16–Mar 15) was 326.71 cents per gallon, corresponding to Level 18 out of 33 tiers (320–329 cents).

This represents an unprecedented 12‑level jump from Level 6 the previous month – the largest monthly increase since the current surcharge system was introduced in 2016.

Korean airlines have raised fuel surcharges on tickets issued this month by up to more than 300%.

Asian jet fuel prices, the benchmark for Singapore averages, reached 522.08 cents per gallon on March 31 – exceeding the top surcharge tier of 470+ cents (Level 33).

If this trend holds through April 15, May will mark the first time surcharges reach the maximum Level 33.

At Level 33:

- US route fuel surcharges will surge from around KRW 300,000 one-way to the mid‑KRW 550,000 range.

- Short-haul surcharges are expected to rise to roughly KRW 100,000.

An industry official commented:

“Even now, surcharges cover less than half of the fuel price increase. If they rise further in the peak May season, it could choke demand and widen losses. The more planes we fly, the more we lose, and service cancellations may expand.”

Most Korean carriers – including Asiana Airlines, Jin Air, Air Busan, and Air Premia – have already reduced unprofitable routes this month.

Share this article :

top