The Power of Logistics to Move the World!

It's the Power of extrans.

EXTRANS GLOBAL - Air Freight News - Week 11 2026

Air Cargo Market Highlights

1) Rate Hikes Inevitable for Korea–Europe Air Cargo – Rising Share of Direct Cargo Flights

The recent near‑wartime situation in the Middle East and subsequent airline suspensions have sharply increased risks of extended transit times and rate rises in the global air cargo market. Due to immediate capacity constraints, rate increases independent of demand are becoming highly likely.

This crisis is not limited to the Middle East; it creates major uncertainty for shippers, airlines, shipping lines, and freight forwarders serving Asia (including Australia) and Europe. Aircraft repositioning, longer routings via detours, and partial suspension of direct services will tighten available air cargo capacity across major trade lanes.

Capacity constraints are already materializing, especially on Far East–Europe and Asia–Middle East corridors. Some carriers have introduced war risk surcharges, with potential +10% additional fees for cargo transiting Middle Eastern airspace or hubs. A silver lining is that China’s export sector has not yet fully recovered production after the New Year holiday.

However, if instability persists for several weeks, China‑origin air cargo rates will rise sharply. Korea faces a similar situation and is scrambling for alternatives amid confirmed flight cancellations to the Middle East.

Currently, Korea–Europe air cargo moves via three main channels:

- Direct routes (Incheon–Frankfurt, Amsterdam, Paris, etc.)

- Transshipment via Gulf (Middle East) hubs

- Routes via Turkey or Central Asia

The most direct impact is on transshipment cargo via Middle Eastern hubs—not direct demand to the Middle East. Cargo from Incheon transiting Doha, Dubai, and Abu Dhabi to Europe now faces high risks of cancellation or delay. Some competitively priced Europe‑bound capacity has effectively disappeared.

Several airlines are adjusting tech‑stop strategies and shifting to direct or alternative routings to Europe. A resumption of polar routing from Korea, Japan, and Taiwan to Europe is also expected.

2) Global Air Cargo Plunges 22% – Middle East Logistics Crisis Puts Korea’s Semiconductor & IT Exports on Emergency Alert

Deliveries halted from fresh produce to aircraft parts. Southeast Asia–Europe rates up over 6%. Incheon–Dubai direct flights suspended; detours risk 80% surge in domestic logistics costs. Disruptions to critical raw materials including helium, plus a chain reaction across industries from soaring oil prices.

Shipments from fresh produce to precision aircraft components are stuck. Global air cargo capacity has dropped by more than one‑fifth, with freight rates rising sharply. Key global logistics hubs in Doha (Qatar) and Dubai (UAE) are paralyzed, causing massive disruptions to global supply chains.

- Deliveries halted from fresh produce to aircraft parts; Southeast Asia–Europe rates up over 6%

- Incheon–Dubai direct flights suspended; detours risk 80% surge in Korean logistics costs

- Supply disruptions for critical materials such as helium, and expected knock‑on industry damage from surging oil prices

Industries including semiconductors and smartphones, which rely on air freight for over 90% of transport, face direct route disruptions and strong upward rate pressure from a worldwide aircraft shortage.

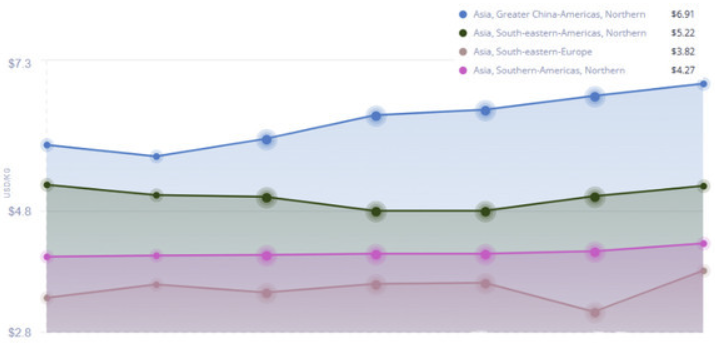

3) Middle East Conflict Cuts Europe Route Capacity by 40%, Rates Surge

Air Cargo Rate Changes by Lane Since Middle East Tensions (unit: $/kg)

Blocked Middle Eastern air routes have cut Asia–Europe air cargo capacity by nearly 40%, sending rates soaring. According to the Freightsos Airfreight Index (FAI):

- China–North America: $6.39/kg (+2% WoW)

- China–Northern Europe: $3.49/kg (+7% WoW)

Compared to pre‑Chinese New Year levels, air cargo capacity (Available Cargo Tonne Kilometers, ACTK) on Asia–Middle East and Southeast Asia–Europe lanes has plunged 39%. This is due to the full closure of key intermediate hubs: Doha (DOH), Dubai (DXB), Abu Dhabi (AUH).

Major carriers representing about 13% of global air cargo capacity—Qatar Airways (QR), Emirates (EK), Etihad (EY)—have effectively suspended cargo services.

Since the conflict began:

- Middle East air cargo capacity down ~80%

- Southeast Asia down ~33%

- Central Asia down ~30%

By contrast, direct Asia–Europe capacity has risen about 13–14% compared to pre‑crisis levels.

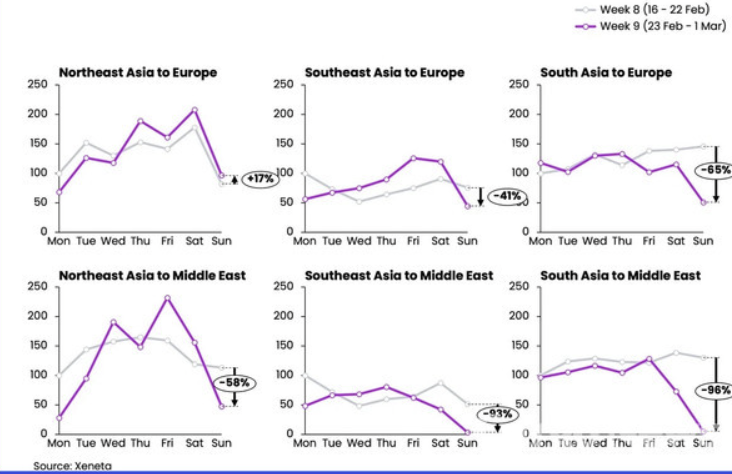

4) Northeast Asia–Europe Rates Surge 17% After Middle East Escalation

Following the U.S. and Israeli military strikes on Iran, most routes saw airfreight rates plunge—but Northeast Asia–Europe jumped 17%.

According to rate analysis by eneta (chargeable weight, index: Feb 16 = 100):

- Southeast Asia–Middle East: -96%

- South Asia–Middle East: -93%

- South Asia–Europe: -65%

- Northeast Asia–Middle East: -58%

- Southeast Asia–Europe: -41%

The real risk lies ahead. Ocean freight—the main alternative to air cargo—faces even greater security risks. With few viable alternatives, air cargo rates have a very high chance of rebounding sharply.

If some ocean cargo shifts to air, Asia–Europe air freight rates—already facing nearly 50% capacity cuts—could enter a new “big bang” era of explosive growth.

Share this article :

top