The Power of Logistics to Move the World!

It's the Power of extrans.

EXTRANS GLOBAL - Air Freight News - Week 50 2024

Air Cargo General

1) Korean Air and Asiana Integration Round 2 – The Competition Among LCCs Begins.

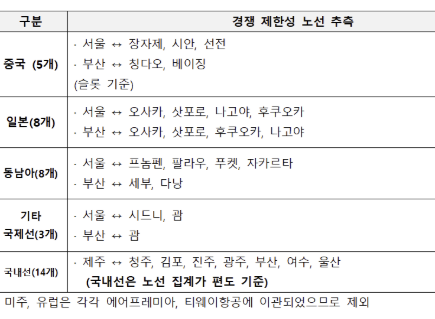

- The merger of Korean Air and Asiana Airlines will result in five companies (Big 2, Jin Air, Air Seoul, and Air Busan) operating a total of 22 international routes and 14 domestic routes.

- The Fair Trade Commission plans to finalize the merger approval on the 11th, coinciding with Korean Air's acquisition of new shares, and will hold an implementation oversight committee within three months to review existing approval conditions. Given the intertwined conditional approvals from various regulatory authorities, it is expected that route adjustments will occur soon.

- The domestic aviation industry believes that the route adjustments should focus on domestic LCCs (low-cost carriers) to resolve monopoly issues among the five companies belonging to Big 2 as quickly as possible.

- If the routes are redistributed to LCCs, the market share of the five companies under Big 2 will decrease rapidly. For example, in the case of Chinese routes, the current market share of 79% will drop to 53.6%, a decrease of 25.4 percentage points.An LCC industry insider stated, “In the past, some routes operated by existing airlines had fares ranging from 1.1 to 1.6 million won, but if LCCs operate these routes, the prices could significantly drop to 600,000 to 700,000 won, which could be beneficial for consumers. If LCCs take over the routes, it will also have a positive effect on revitalizing the aviation market.”

- If a large LCC emerges from the integration of LCCs under Big 2 (Jin Air, Air Seoul, Air Busan), it could lead to significant changes in the rankings of the top three carriers. Currently, Jeju Air has 41 aircraft, but the combined LCC could theoretically rise to 58 aircraft. This puts pressure on existing companies to develop strategies to recover.

- At this point, where the number of operators for mid- to short-haul routes has increased and become saturated, it is essential for other companies that have felt constraints on new business due to the delays in the Big 2 merger.

- Excluding those under Big 2, there are currently five LCCs operating (Jeju Air, T'way Air, Eastar Jet, Air Premia, and Air Loke). Recently, Parata Air, which emerged from the acquisition of Fly Gangwon, has opened an office near Gimpo Airport, and High Air, which previously operated routes from regional airports like Sacheon Airport, is reportedly seeking to re-enter the market. The routes offered by the five companies under Big 2 will inevitably attract attention as these LCCs solidify their intentions for business expansion.Therefore, a fierce competition is expected among LCCs to secure the routes offered by the five companies under Big 2.

2) IATA Announcement - Air Cargo Demand Increases for 15 Consecutive Months, but Market Outlook for Next Year is Uncertain.

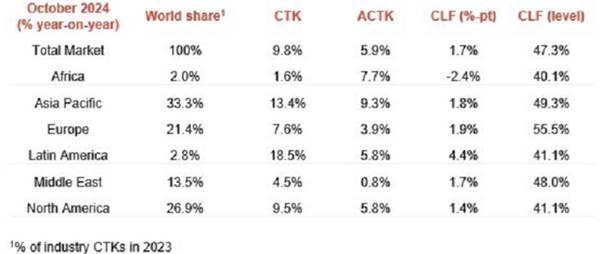

- According to statistics released by IATA (International Air Transport Association) for October, air cargo demand increased by 9.8% compared to the same period last year, continuing a 15-month upward trend.

- In October, global air cargo capacity (Available CTK) increased by 5.9%, and the cargo load factor rose by 1.7 percentage points to 47.3%.

- This increase in capacity was primarily due to an 8.5% rise in bellyhold capacity from passenger aircraft and a 5.6% increase in freighter capacity. The supply from freighters is nearing the highest level seen in 2021.

- IATA's Director General Willie Walsh stated, "In 2024, air cargo yields are expected to increase by 10.6% compared to 2023 and by 49% compared to 2019." He added, "2024 is expected to be an important year for the air cargo industry, but caution is needed for 2025."

- Meanwhile, IATA recently analyzed several market indicators and highlighted the following:

- Global industrial production increased by 1.6% in September, and global merchandise trade rose by 2.4%, marking six consecutive months of growth.

- The Purchasing Managers' Index (PMI) for global manufacturing production remains above 50, indicating ongoing growth.

- The new export orders index is below 50, suggesting trade uncertainty and weakness.

- By region, air cargo demand from Asia-Pacific airlines in October increased by 13.4% compared to the previous year, showing the most notable performance, with capacity rising by 9.3%.

- North America: Demand increased by 9.5%, and capacity rose by 5.8%.

- Europe: Demand increased by 7.6%, and capacity rose by 3.9%.

- Middle East: Demand increased by 4.5%, and capacity rose by 0.8%.

- Latin America: Demand increased by 18.5% (the highest growth rate), and capacity rose by 5.8%.

- Africa: Demand increased by 1.6% (the lowest growth rate), and capacity rose by 7.7%.

3) CAAC Announces Record High for Air Cargo from China - Cumulative Total of 7.3 Million Tons in October (Up 19.3% Compared to 2019).

- Recently, the Civil Aviation Administration of China (CAAC) announced that the air cargo volume from China in 2024 has reached a "historical high."

- The CAAC stated that approximately 7.3 million tons of cargo and mail were transported from January to October, which represents a 19.3% increase compared to 2019.

- This "historical peak" was attributed to the "strong growth" of international air cargo. The volume of international flights heading to export destinations surged by 48.5% to reach 2.93 million tons.

- In the last week of November, cargo flights heading to international destinations grew by 100.4% compared to the previous year. This growth is largely attributed to China's industrial transformation, closer cooperation along the Belt and Road Initiative, and the rapid development of cross-border e-commerce.

- However, concerns have been raised about the long-term outlook for China's air cargo transport sector due to escalating tariff conflicts since Donald Trump's presidency. There are particular worries that e-commerce may be at risk, as over one-third (35%) of China's e-commerce volume is currently transported to the United States via air. The remaining 25% primarily goes to Europe, mainly through Germany.

- Meanwhile, Boeing recently projected in its 2024 Commercial Market Outlook (CMO) that the number of cargo aircraft in China will nearly triple by 2043, driven by demand from the booming e-commerce sector. It is expected that 170 dedicated cargo planes will be delivered to China from 2024 to 2043, including both new and converted models.

4) Although there is a surge in air cargo from China, we must act quickly before Trump's return.

- As Donald Trump prepares to return to the White House, U.S. companies are rushing to secure imports from China to avoid tariffs. Consequently, air cargo from China has also surged.

- According to Bloomberg News on the 28th (local time), there were 3,485 international cargo flights between China and other countries last week.

- This is the highest number since China lifted its COVID-19 lockdown measures in March 2023. The Chinese Ministry of Transport reported that the number of weekly flights has exceeded 3,400 for three consecutive weeks.

- From January to October this year, the number of cargo flights increased by 73% compared to the same period last year. The number of ships transporting goods to China rose by 8.3%. Truck and rail transport also saw double-digit growth.

- With Trump's return to the White House imminent, air cargo is expected to increase further. Trump announced on the 25th that he would impose an additional 25% tariff on imports from Mexico and Canada, and a 10% tariff on imports from China. During his campaign, he repeatedly stated that he would impose a universal tariff of 60% on Chinese imports.

- Bloomberg noted that "as Trump is set to take office at the end of January, U.S. companies are likely to increase their purchases as much as possible before he imposes new tariffs on goods from China, Mexico, Canada, and other countries, potentially leading to an increase in the number of flights."

5) GSA and Airline Trends

- From January 1 next year, Mersk Air Cargo will operate cargo flights on the CGO-ICN-GSP route with a B777F.

- Hawaiian Airlines will operate direct passenger flights from ICN to SEA four times a week starting next October.

- Scandinavian Airlines (SK) will operate direct passenger flights from ICN to COP four times a week starting next September.

Share this article :

top