The Power of Logistics to Move the World!

It's the Power of extrans.

EXTRANS GLOBAL - Air Freight News - Week 19 2026

Air Cargo Market Overview

1) Air Cargo Market: Freight Forwarder Market Update

Persistent Supply & Demand Pressure

- China to US air cargo demand remains strong, driven by AI server equipment, e‑commerce volumes, sea-to-air cargo diversion, and rising general cargo shipments.

- Sustained robust demand keeps air cargo capacity tight, supporting elevated freight rates.

- Market expectations were for capacity pressure to ease during China’s Labor Day holiday; however, rates have continued rising despite steady demand to Europe.

- Most Asia Pacific markets are forecast to maintain strong demand and tight capacity, accompanied by persistently high freight rates and longer transit lead times.

Freight Rate & Market Outlook

- Although the pace of rate hikes has slowed compared with the early stage of the Middle East conflict, the overall upward trend in air cargo rates remains intact.

- Renewed risks of Strait of Hormuz closure, rising jet fuel prices, and prolonged geopolitical tensions are likely to keep spot freight rates elevated in the near term.

- Additional rate increases are possible in the coming weeks due to higher jet fuel costs and constrained capacity availability.

2) Worst-Case Scenario Averted After April Air Cargo Rate Surge

Market conditions are expected to remain challenging through year-end amid persistent inflation and a 9% year-on-year drop in China cross-border e-commerce volumes as of March.

Some cargo may have shifted to air consolidation services and been excluded from official statistics. Nevertheless, the downward trend in China-origin volumes over the past four months clearly confirms slowing growth in B2C e-commerce air cargo demand.

Recent market movements reflect a generally pessimistic outlook for the 2026 logistics sector.

Global air cargo rates have likely peaked, with downward corrections expected across more routes going forward.

Concerns over supply chain disruptions and trade uncertainty persist, leaving market direction highly uncertain.

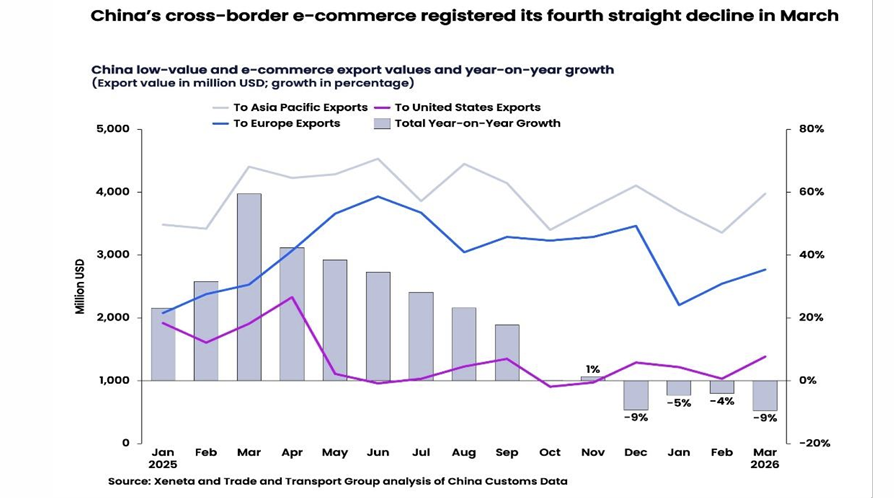

China Cross-Border E-Commerce Declines for 4 Consecutive Months through March

- China’s cross-border e-commerce export growth slowed from mid-2025 and turned negative toward late 2025.

- Year-on-year growth slipped after hitting +1% in October 2025, falling to -9% in March 2026, marking four straight months of decline.

- Volumes to Asia Pacific lead the overall trend; US-bound cargo dropped sharply and remains at a low level, while Europe-bound volumes have rebounded slightly recently.

- Overall, export growth has ended following the 2025 peak, entering a clear contraction phase.

3) May International Fuel Surcharge Set at Maximum Tier – Long-Haul Rate at KRW 2,260/kg

Korean Air officially announced cargo fuel surcharges effective May 16, set at the highest Tier 34 level.

Based on chargeable weight:

- Long-haul routes: KRW 2,260/kg

- Mid-haul routes: KRW 2,120/kg

- Short-haul routes: KRW 2,020/kg

As widely anticipated, the May fuel surcharge has reached the current regulatory ceiling.

Market consensus expects further upward pressure on cargo rates, while some industry participants believe rates will gradually adjust to absorb higher surcharge costs.

A key concern remains whether additional hikes will be possible in June should international oil prices rise further.

Critics point out structural flaws in Korea’s fixed price-bracket fuel surcharge system, calling for a full review and revision of the surcharge framework.

4) Limited Rate Hikes Despite Renewed Middle East Tensions – Global Air Cargo Enters Stabilization Phase

Fuel cost inflation and ongoing supply chain uncertainty continue to squeeze profitability across air and ocean logistics sectors; however, markets have largely priced in geopolitical risks and entered a stabilization period.

According to Freightos’ weekly market update, air cargo market movements have stayed within recent ranges over the past few weeks.

Air cargo fundamentals remain steady. High jet fuel prices, gradual capacity recovery, and demand concentration toward Middle East-linked routes keep rates elevated, yet most lanes have passed their peak and entered a consolidation phase.

The Freightos Air Index global benchmark remains roughly 25% above pre-conflict levels but fell 5% month-on-month.

China–US rates stand at $5.48/kg, down 7% from late February; most major routes have also retreated from mid-April highs.

By contrast, Middle East-bound air cargo remains under strong pressure:

- North America–Middle East: $4.57/kg, up 6% week-on-week, hitting an all-time high.

- Europe–Middle East: $3.87/kg, only 2% below the record set two weeks ago.

This trend is attributed to recovering air capacity in the Middle East paired with rising regional demand.

While global logistics markets have partially priced in Middle East conflict risks, oversupply and sluggish demand remain key factors limiting further rate inflation.

Industry analysis notes that global economic slowdown and weakening consumption are more likely to shape future market trends than Middle East geopolitical tensions alone.

Separately, the planned Trump–Xi summit aimed at stabilizing US–China trade relations faces potential disruption from Middle East developments.

Diplomatic tensions have flared again following China’s opposition to new US sanctions targeting Iranian crude oil imports.

Share this article :

top