The Power of Logistics to Move the World!

It's the Power of extrans.

EXTRANS GLOBAL - Air Freight News - Week 14 2026

Air Cargo Market Highlights

1) Logistics Bottlenecks Persist Despite Partial Reopening of Strait of Hormuz

Although geopolitical risks in the Middle East show some signs of easing, the global logistics market still faces high uncertainty and cost pressure. While ocean freight has seen only limited normalization, air cargo markets remain strong on rates amid capacity constraints.

In its weekly update, Freightos noted that Iran has recently allowed limited vessel traffic through the closed Strait of Hormuz, providing some relief to Middle Eastern maritime logistics. However, this is more of a conditional passage than full normalization, with access limited to certain cooperating countries or vessels paying transit fees.

Cargo in the Gulf region is partially moving via alternative ports and land bridges, but bottlenecks are worsening. Structural issues such as vessel congestion, truck shortages, insufficient road infrastructure, and border delays are prolonging transit times.

The air cargo market shows a different trend: Middle Eastern carriers are gradually normalizing operations. Emirates SkyCargo stated it has entered a stabilization phase, and Qatar Airways Cargo has also begun a late recovery.

Nevertheless, global capacity remains tight. Much of the Asia‑origin cargo is bypassing Gulf hubs and rerouting via the Far East, reducing network efficiency. Despite lower year‑on‑year demand, rates are still rising. On some routes, fuel surcharges have reached $2 per kg.

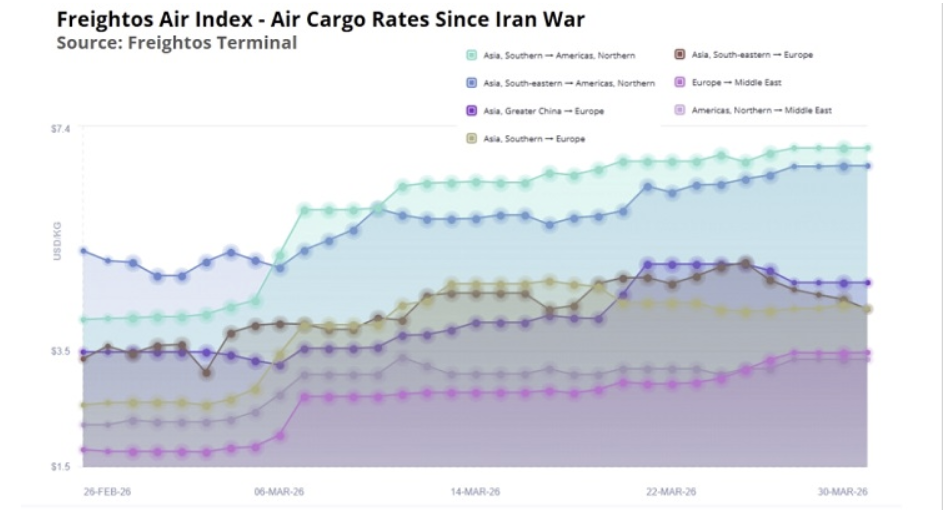

Global air rates as measured by the Freightos Air Index are 22% higher year‑on‑year. Key routes:

- South Asia–Europe: +65% vs February, -1% week‑on‑week

- Southeast Asia–Europe: +26% vs pre‑conflict, -6% week‑on‑week

This is attributed to expanded direct services by European and Far Eastern carriers and the partial recovery of Middle Eastern airlines.

2) Prolonged Iran Conflict Triggers Fresh Surge in Air Cargo Rates

Global air cargo rates have risen sharply again amid the prolonged Middle East conflict and ongoing air supply chain disruptions.

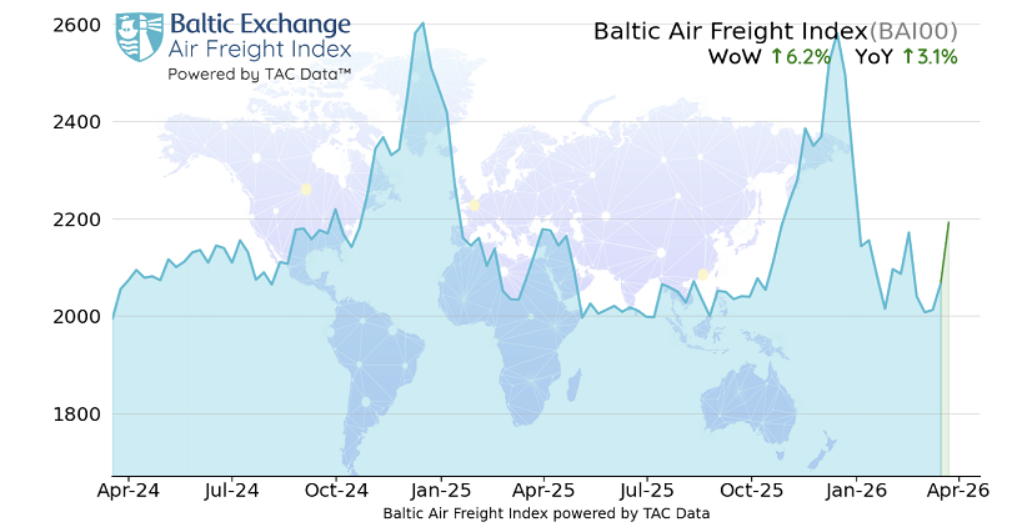

According to the TAC Index, upward pressure intensified last week due to a combination of soaring fuel costs and operational disruptions.

The Baltic Air Freight Index (BAI00) compiled by TAC rose +6.2% week‑on‑week and +3.1% year‑on‑year as of March 23.

Alongside rate increases, jet fuel prices have more than doubled in the past month, leading to the rapid spread of fuel surcharges — a key driver of the price rally.

Rates rose strongly across major Asian origins. China‑origin routes to Europe and North America both increased; Hong Kong spot rates neared peak‑season levels, with larger gains in India and Korea.

- Hong Kong overall index (BAI30): +3.7% WoW, +2.5% YoY

- Shanghai index (BAI80): +13.9% WoW, +5.4% YoY

Seoul, Bangkok, and India also posted strong weekly gains. India in particular saw severe tightening due to fewer flights via the Middle East, reducing both belly and freighter capacity. Taiwan also trended higher.

Vietnam edged down week‑on‑week but remained elevated YoY on European routes.

Europe‑origin rates also rose on most major lanes, including transatlantic services to the U.S. and routes to China, Japan, India, Australia, Mexico, and South Africa. North America was mixed: rates rose to China and Asia but fell to Europe and South America.

3) Asia Pacific Market Trend Summary

Asia Pacific → Europe spot rates: +8% WoW, average above $5/kg, +26% YoY

Key Features

- Stronger demand and persistent space shortages across most major origin markets

- Week 12 capacity +3% WoW (driven by freighter expansion)

- Airlines and forwarders working to address supply shortages in key markets

Operating Environment

- Ongoing impact of airspace and airport restrictions in the Gulf region

- Rising jet fuel prices and fuel supply shortages in some countries

- Additional operational constraints emerging in parts of Asia

Outlook

- Strong demand, capacity constraints, and rising costs to continue; further upward pressure on spot rates

Gulf Aviation Market Recovery & Stabilization

- After sharp declines and rapid recovery following the Middle East conflict, Gulf carriers have now entered a new stabilization phase

- Most airlines have maintained steady daily flight numbers over the past five days

- The post‑collapse rebound has concluded, with the market reaching a balanced range for stable network operations

4) Middle East Risks Spark Surge in Charter Costs – Supply‑Driven Air Cargo Rally Intensifies

Heightened geopolitical risk in the Middle East has sent air cargo charter rates soaring. A perfect storm of rising jet fuel prices, scarce aircraft capacity, and fuel supply instability has driven abnormal increases in charter costs.

Current charter rates are now comparable to levels seen during the COVID‑19 pandemic. However, unlike that period, the market is being driven by supply constraints rather than demand growth, creating a major structural difference.

A charter operator commented that even outside the traditional peak season, fuel costs are artificially inflating rates, with current contract levels similar to pandemic highs.

Disruptions to scheduled services due to Middle Eastern airspace risks have shifted significant volumes to charters, causing a surge in replacement demand. Major Gulf carriers including Etihad, Qatar Airways, and Emirates — which provide a large share of global air cargo capacity — have faced operational disruptions, directly reducing global supply and pushing up charter rates.

The market faces a triple whammy: soaring jet fuel costs, reduced capacity from Middle Eastern carriers, and increased fuel price volatility amplifying uncertainty around fuel surcharges.

Demand remains relatively robust, with high inquiry levels for charters but low conversion to actual contracts, as rates exceed what shippers are willing to pay.

Experts warn that prolonged price pressure — including market rates and charter costs — will likely lead to softer cargo volumes from shippers.

Share this article :

top