The Power of Logistics to Move the World!

It's the Power of extrans.

EXTRANS GLOBAL - Air Freight News - Week 13 2026

Air Cargo Market Highlights

1) US-Iran War and the Air Cargo Market – Profitability Worsens as War Hits Low Season (Jan–Feb)

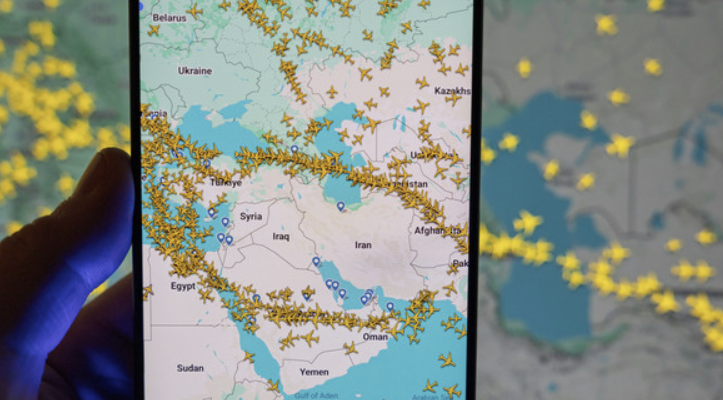

The air cargo market is struggling amid the US-Iran conflict, with major airports in the Middle East closed or operating at reduced frequencies.

Airports in Iran, UAE, Qatar, Bahrain, Kuwait, and Iraq have all been affected, including Dubai International Airport and Hamad International Airport – key global and regional air cargo hubs – which are facing severe operational disruptions.

Freight rates have surged sharply. Middle Eastern carriers act as critical hubs connecting Asia, Europe, and Africa. As airport operations faltered and flight frequencies dropped, long-haul routes including Europe-Middle East lanes saw rates rise 10–20% immediately after the conflict, then jump more than 50% entering the second week.

Korean and international airlines are also within the crisis zone. Carriers including Korean Air have drastically reduced flights to Iran and other Middle Eastern destinations.

An air cargo industry official commented:

“January and February are traditionally a low season for air cargo, so we had prepared to some extent. But once the war started, the situation spiraled out of control.

Volumes are down by at least 20% and up to more than 40% compared to previous years. We pretend to be calm outwardly, but we are burning up inside.”

Airlines have traditionally addressed oil price spikes by imposing fuel surcharges, and large-scale increases from April are now unavoidable.

Industry forecasts suggest rates on North America routes could rise from KRW 1,800 per kg to above KRW 2,000 in the early range.

2) Summer Flight Schedule Finalized – International Routes Expanded, Regional Connectivity Strengthened

The Ministry of Land, Infrastructure and Transport has finalized the 2026 summer regular flight schedule, featuring expanded international services, stronger regional airport links, and the planned new Incheon–Jeju route, which will improve passenger convenience and broaden service options.

For the summer season starting March 29, international services will cover 245 routes with a maximum of 4,820 weekly flights – an increase of 37 flights (0.8%) compared to summer 2025.

Notable new and resuming routes include Jin Air’s new Busan–Miyakojima service, plus the restart of routes suspended in winter: Incheon–Montreal (Air Canada), Calgary (WestJet), and Zagreb (T’way Air).

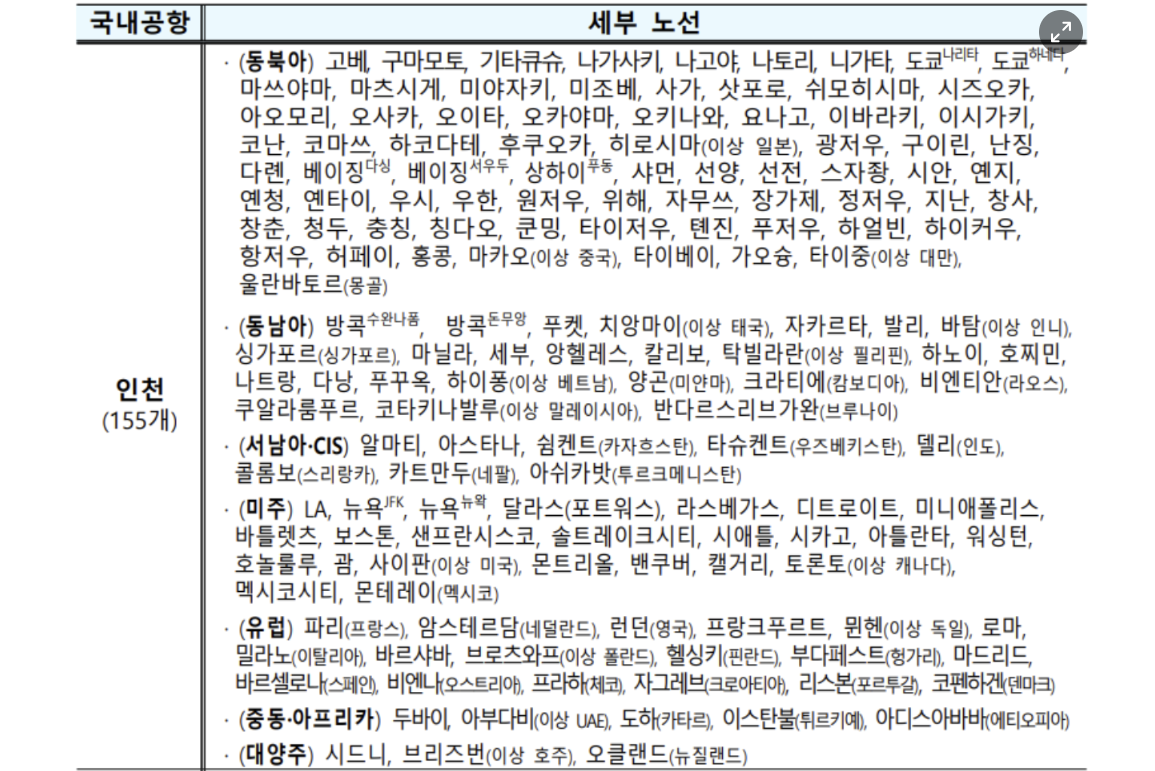

Incheon International Airport will operate 155 routes, reinforcing its global hub status covering the Americas, Europe, Middle East, and Oceania, with balanced long-haul core routes to Los Angeles, New York, London, Paris, etc., maintaining strong transfer competitiveness.

Key trends in the summer schedule include:

- Expanded long-haul networks centered on Incheon

- Southeast Asia and Japan-focused capacity at regional airports

- Gradual recovery of China routes

The industry expects supply expansion to meet peak-season demand alongside intensifying route competition.

An MOLIT official noted that from this summer, LCCs selected as replacement carriers following the Korean Air–Asiana Airlines merger will be deployed on selected routes.

3) Parata Air Launches New Incheon–Hanoi Route – Targeting Business and Cargo Demand

Parata Air is launching a new route to Hanoi, Vietnam, to expand its Southeast Asian network.

The carrier aims to diversify its revenue structure by securing a route with strong corporate travel and cargo demand.

On March 19, Parata Air announced it will operate daily Incheon–Hanoi flights starting July 13 using Airbus A330 aircraft.

Schedule:

Departs Incheon International Airport at 19:55, arrives at Hanoi Airport at 22:50 local time.

Return flight departs Hanoi at 00:20 local time, arrives in Incheon at 06:40 Korean time.

As Vietnam’s economic center with a dense concentration of Korean production bases, Hanoi offers steady business demand.

Unlike tourism-focused routes, it is expected to deliver stable profitability driven by consistent corporate travel.

The launch is part of Parata’s fleet expansion strategy. The carrier recently finalized a contract for its 5th aircraft, accelerating mid-to-long haul competitiveness.

The plane will be delivered within the first half of the year and used for further route expansion.

Parata Air has introduced four aircraft since its first in July last year and is in negotiations for additional deliveries.

4) Fears of Prolonged Middle East Risk Drive Air Cargo Surge – Rates Rise Across Asia and Europe (TAC Index)

Global air cargo rates have rebounded sharply amid prolonged Middle East conflict and ongoing supply chain disruptions.

According to TAC Index, upward pressure intensified last week due to a combination of soaring fuel costs and operational disruptions.

The Baltic Air Freight Index (BAI00) rose 6.2% week-on-week as of March 23 and stood 3.1% higher than the previous year.

Alongside rate increases, jet fuel prices have more than doubled in the past month, leading to the rapid spread of fuel surcharges – a key driver of the freight rate rally.

Rates have strengthened broadly across major Asian origins.

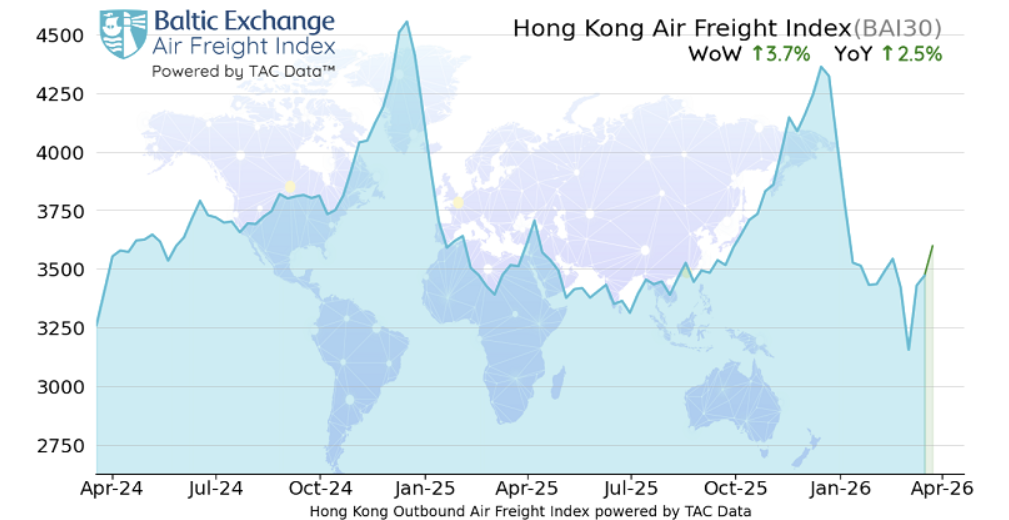

China-origin routes to Europe and North America both rose; Hong Kong spot rates neared peak-season levels, with sharp increases also seen in India and Korea.

Hong Kong overall index (BAI30) rose 3.7% week-on-week, while Shanghai index (BAI80) surged 13.9%.

Seoul, Bangkok, and India also posted strong weekly gains.

India in particular has seen severe market tightening due to fewer flights via the Middle East, reducing both belly and freighter capacity simultaneously. Taiwan also trended upward.

Vietnam edged down week-on-week but remained above year-ago levels on European routes.

Experts interpret this rally not as a simple peak-season effect but as a structural shock chain:

Middle East airspace closure → capacity contraction → fuel cost surge → wider surcharges.

As Asia-origin volume concentrates toward Europe and North America, increased detour routing and lower aircraft utilization are further tightening the market.

Middle East airspace closure → capacity contraction → fuel cost surge → wider surcharges.

Share this article :

top