The Power of Logistics to Move the World!

It's the Power of extrans.

EXTRANS GLOBAL - Air Freight News - Week 23 2026

Air Cargo Market Highlights

1. South Korea-China Cargo Hub Routes: Weekly Flight Rights Increased by 14

Following aviation talks between South Korea and China, the Ministry of Land, Infrastructure and Transport has reached an agreement to expand flight rights between the two countries for the first time in seven years, opening up new growth opportunities for both passenger and air cargo sectors. The additional cargo flight rights connecting major cargo hub airports in China are expected to strengthen bilateral logistics networks and improve transportation efficiency for import and export enterprises.

Under the deal, weekly passenger flights rise from 608 to 664, a net increase of 56. Weekly cargo flights are expanded from 54 to 68, adding 14 weekly services. Connectivity between South Korean airports and key Chinese cargo hubs has been significantly enhanced.

The 14 extra weekly cargo routes link South Korea with major Chinese freight airports including Tianjin, Zhengzhou, Ezhou and Hefei. Industry insiders comment that rising volumes of cross-border e-commerce shipments and growing demand for air freight related to semiconductors, batteries and advanced manufacturing products will make the expanded flight rights a strong boost to logistics competitiveness on both sides. The reinforced direct cargo network connecting production bases in central and western China with South Korea is also set to encourage airlines to launch new cargo routes.

2. Weekly Air Market Update: Slow Capacity Recovery

Global Air Cargo Capacity Trend

- Global air cargo capacity rose by approximately 1% week-on-week.

- Dedicated freighter capacity remained stable, while bellyhold capacity on passenger aircraft increased by 2% week-on-week.

- Among all major global regions, the Middle East & South Asia (MESA) posted the largest week-on-week capacity growth in Week 21, with a further 5% recovery.

- Even so, regional capacity is still around 32% lower compared with pre-conflict levels in Week 7, a drop of nearly one-third.

- Capacity across the Gulf region has fallen by 48%, less than half of its pre-conflict volume. The figures indicate that a substantial expansion of Gulf air cargo capacity remains challenging amid ongoing market instability.

- Meanwhile, carriers outside the Gulf region continue to ramp up dedicated freighter deployments.

Year-on-Year Capacity Comparison

- Global air cargo capacity is up roughly 3% year-on-year for the current week.

- Given persistent capacity shortages across Gulf airlines and the wider Gulf area, the 3% year-on-year growth appears unexpected.

- Nevertheless, this growth rate is less than half of the figure recorded in the first two months of 2026, before the outbreak of tensions between the US and Iran.

3. AI and Semiconductors Drive Strong Air Cargo Performance

Growing global investment in semiconductors and AI infrastructure has become a core growth engine for Asia’s air cargo market. Soaring exports of semiconductors and AI servers, mainly from Taiwan and South Korea, have aggravated capacity tightness and pushed up freight rates on key trade lanes.

Major Asian economies together with the US register solid manufacturing expansion: Taiwan (55.3), South Korea (53.6), the US (54.5) and mainland China (52.6). Production activities in Taiwan and South Korea have improved markedly, fuelled by robust outbound shipments of AI servers and semiconductors.

In South Korea, capacity constraints are expected to persist, driven by rising cross-border e-commerce cargo and transit freight from China to the US via Incheon Airport, as well as ongoing modal shifts from ocean to air transport.

Routes from South Korea to Singapore, Penang and Kuala Lumpur face extreme capacity pressure and volatile rates due to surging demand for semiconductor equipment shipments. The load factor of overnight flights to Europe also exceeds 95%.

Jet fuel shortages are another key cause of tight capacity. Reports note that more airlines are adopting fuel-saving measures, such as imposing cargo weight limits and replacing Boeing 747 freighters with Boeing 777 units. As a result, actual effective capacity has declined sharply, even though overall market demand remains comparable to last year’s level.

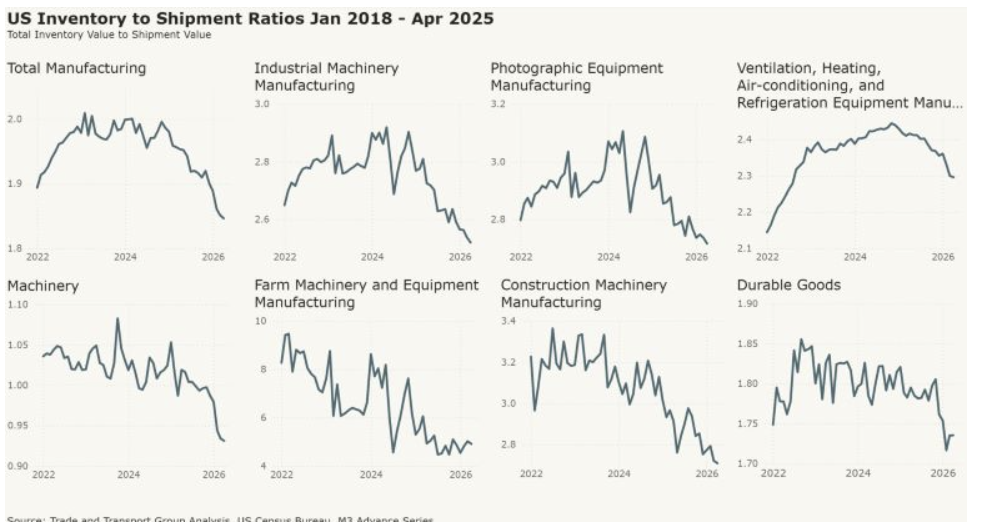

4. Falling US Inventory-to-Shipment Ratio Raises Hopes for Air Cargo Recovery

Declining Inventory-to-Shipment Ratio

The continuous drop in the US inventory-to-shipment ratio sends a positive signal to the air cargo industry. According to the latest M3 Advance data released by the US Census Bureau and analysed by logistics research firm Trade and Transport Group, the overall manufacturing inventory-to-shipment ratio stood at around 1.83 in April 2025, down notably from the peak recorded between 2022 and 2023.

Outbound Shipments Outpace Inventory Build-up

Over the past few months, shipment growth has outpaced inventory growth. A falling inventory coverage ratio generally bodes well for air freight: shorter inventory cycles mean companies are likely to ramp up urgent replenishment orders to fulfil future demand. As air transport offers shorter lead times, the entire air cargo market is expected to benefit from rising shipment volumes.

Drawdown of Pre-emptive Stockpiles

Some market observers argue the falling ratio also reflects the end of front-loading activity, where businesses built up inventories in advance ahead of the Trump administration’s new tariff policies. Post front-loading, rapid inventory depletion has dragged the ratio lower. Air cargo saw a temporary demand spike earlier this year over tariff concerns, and subsequent cargo trends remain under close watch.

Recovery Prospects for Peak Season in H2

Industry experts forecast that if the inventory-to-shipment ratio keeps declining, the air cargo market will gain stronger recovery momentum in the second half of the year, coinciding with the traditional peak shipping season.

Share this article :

top