The Power of Logistics to Move the World!

It's the Power of extrans.

EXTRANS GLOBAL - Air Freight News - Week 22 2026

Air Cargo Market Highlights

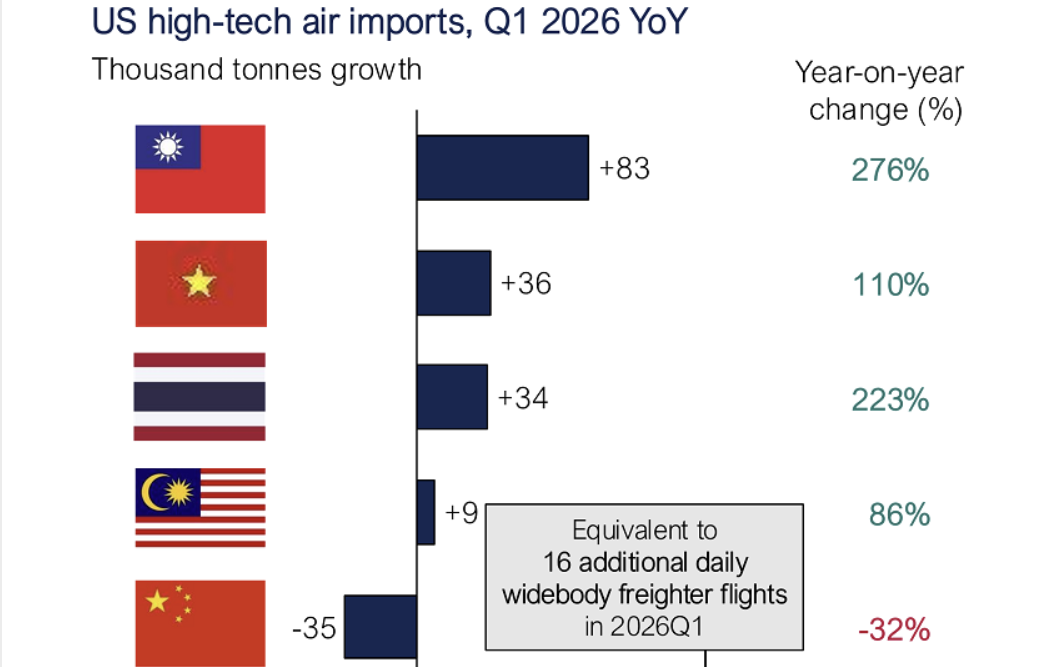

1. Asia-origin High-tech Air Shipments to US Surge 57% in Q1

Based on its proprietary trade database, logistics consultancy Aevean released analysis on May 18 showing U.S. air import volumes of high-tech goods from Asia jumped by 157,000 tonnes (+57%) year-on-year in Q1 2026, equivalent to an extra 16 wide-body freighter flights operated every single day throughout the quarter.

By origin territory:

Taiwan led the surge with +83,000 tonnes (+276%), followed by Vietnam (+36,000 tonnes, +110%), Thailand (+34,000 tonnes, +223%) and Malaysia (+9,000 tonnes, +86%). In contrast, mainland China’s volumes dropped 35,000 tonnes (-32%).

Notably, Taiwan’s incremental cargo volume was more than double mainland China’s cargo decline.

Taiwan led the surge with +83,000 tonnes (+276%), followed by Vietnam (+36,000 tonnes, +110%), Thailand (+34,000 tonnes, +223%) and Malaysia (+9,000 tonnes, +86%). In contrast, mainland China’s volumes dropped 35,000 tonnes (-32%).

The data reflects tangible shifts from U.S. tariff pressures on China and the global China+1 supply chain diversification strategy, prompting relocation of high-tech manufacturing capacity and reshaping Asia-US air cargo flows.

Concentrated semiconductor and electronics production has rapidly turned Taiwan and Southeast Asian hubs into core pillars of transpacific air freight.

Taiwan and Thailand posted triple-digit growth to solidify status as emerging high-tech export bases, while Vietnam also logged steep volume expansion.

2. Further Modal Shift from Air to Ocean Cargo Expected

Air-to-sea conversion picked up in Q1

- In its Q1 2026 earnings call covered by Supply Chain Dive, Matson Logistics confirmed ongoing air-to-ocean cargo diversion and anticipated more volume switching ahead.

- Matson provides integrated rail, truck, ocean transport plus supply chain, logistics and warehousing services.

Higher air rates and constrained capacity drive modal change

Matson’s Chairman & CEO noted sustained air-to-sea shifts amid sky-high airfreight prices and shrinking air capacity, benefiting ocean carriers across multiple trade lanes.

While modal conversion between air and sea is commonplace in logistics, surging jet fuel prices stemming from Middle East tensions and Strait of Hormuz disruptions have accelerated air-to-ocean switching most prominently.

Persistent energy costs keep air cargo market under strain

Prolonged elevated energy prices and capacity constraints will continue to disrupt air freight, with regions reliant on imported jet fuel suffering the worst fallout. Expensive fuel has pushed many shippers to opt for ocean instead of air transport.

That said, the latest TAC Index reports global airfreight rates have softened after the sharp spike triggered by the Middle East conflict.

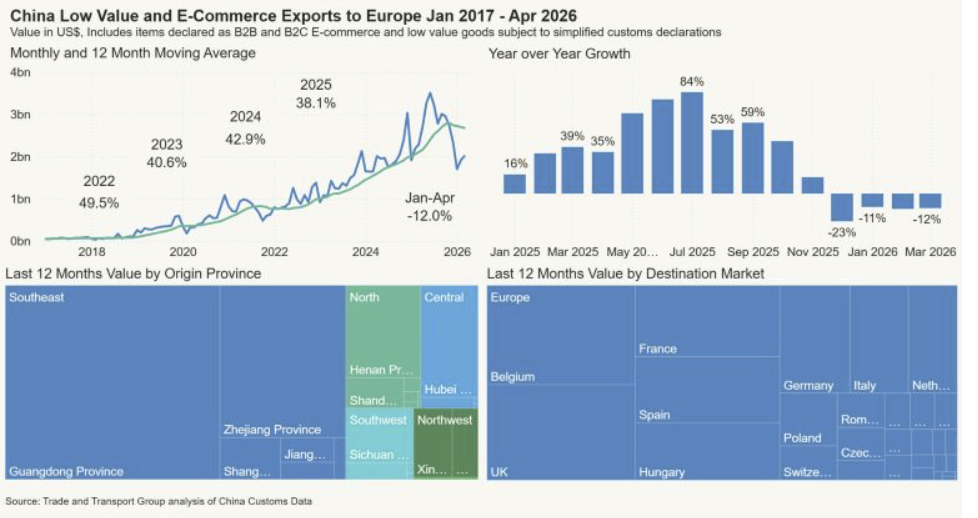

3. China’s E-commerce Exports to Europe Fall for Four Consecutive Months; Only Hungary Posts Positive Growth

China’s cross-border e-commerce shipments to Europe have declined for four straight months with stark country-by-country divergence: Hungary-bound volumes rose by 14%, while Belgium and the UK dipped moderately by 3% and 4% respectively.

Major European consumer markets recorded sharp import falls from China: Germany (-32%), France (-39%), Italy (-21%), Poland (-23%), Spain (-10%) and the Netherlands (-9%).

The downturn stems from tighter EU customs oversight, stricter scrutiny on low-value e-commerce goods and weakening European consumer demand, compounded by new EU regulatory crackdowns targeting affordable Chinese e-commerce platforms.

The shift weighs heavily on Asia-Europe air cargo. Volumes from platforms including Temu and Shein have long underpinned transpacific air freight demand and fuelled robust transit cargo growth at Incheon Airport, which is now facing a rapid demand slump.

Soft spot rates and intensifying bellyhold competition have emerged on multiple lanes, with Incheon’s transshipment business feeling clear market pressure.

Major e-commerce players are expanding alternative logistics via new Eastern European hubs, diverting cargo toward combined air and overland intermodal transport going forward.

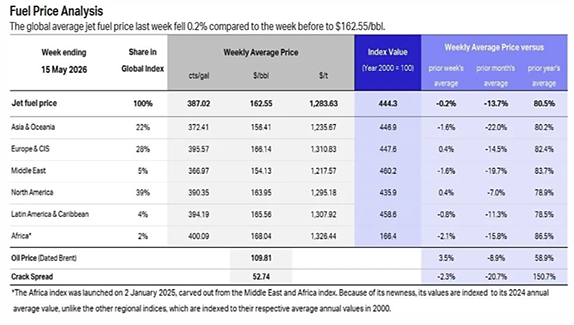

4. Jet Fuel Concerns Ease Yet Air Cargo Settles into High-Cost Regime

The air cargo market has exited acute crisis territory alongside gradual capacity recovery and easing short-term worries over jet fuel shortages. Even so, freight levels remain far above pre-conflict benchmarks with uneven performance across individual routes.

After steep rate hikes following the late-February escalation of Middle East tensions, latest TAC Index data signals market cooling:

- The weekly Baltic Air Freight Index (BAFI) as of May 18 slid 4.9% week-on-week but stayed 0.4% higher year-on-year.

- TAC links the recent rate pullback to a roughly 10% short-term drop in jet fuel prices in early May, though fuel costs still stand 80% above the same period last year.

High operational costs have become the new normal across global air freight.

Share this article :

top