세상을 움직이는 물류의 힘!

바로 엑스트란스의 힘입니다.

엑스트란스 - 항공 물류 업데이트 - 41주차 블로그

1. 항공화물 General

1) 익스프레스/소형 소포 시장은 2030년가지 8% 성장 전망

- 2029년까지 세계 물류시장은 연평균 3.8% 성장할 전망. 특히 아 • 태지역이 연평 균 5.9% 성장하면서 전반적인 상승세를 주도할 전망.

- 또 중동 • 북아프리카(MENA)시 장도 연평균 4.8%의 성장세가 예상.

- 최근 영국 트랜스포테이션 인텔리전스(T'가 전망한 바에 따르면 전체 물류시장 가운데 계약물류시장은 지난 2020~2024년동안 2,469억 유로에서 2,956억 유로시장으로 확대. 아 • 태지역의 계약물류시장은 오는 2029년까지 연평균 6.33% 성장세가 예상.

- 작년 글로벌 포워딩시장은 6.1% 성장했으며, 아 •태지역이 글로벌 포워딩시장의 36.1%를 차지.

- 익스프레스 • 소형 소포시장은 오는 2020년까지 7.9% 성장할 것으로 전망. 2024년 기 준 세계 익스프레스 • 소형 소포시장은 2,727억 유로시장을 형성, 최근 5년 간 가장 빠른 성장세.

- 올해 세계 전자상거래 물류시작은 전년대비 15.5%의 성장세를 보일 전망이며, 작년 기준 북미가 가장 큰 시장으로 2,004억 유로의 시장을 형성.

2) “아시아 환적 허브 ‘과부하’” - 성수기 동남아발 항공화물 수요 압도

- 아시아 항공화물 시장이 성수기 정점을 맞으며 주요 환적 허브들이 극심한 압박을 받고 있다고 Dimerco Express가 10월 시장 보고서에서 밝힘. .

- 9월 말 슈퍼 태풍 ‘라가사(Ragasa)’가 중국 남부와 홍콩을 강타하면서 항공편 결항과 물류 적체가 이어졌고, 여기에 중-유럽 철도 노선의 일시적 운행 중단까지 겹치면서 항공 운송 수요가 폭증했다는 분석.

- 특히 “동남아시아가 수출 수요를 주도하고 있다. 태국, 베트남, 말레이시아, 싱가포르 등에서 출발하는 AI·반도체·이커머스 화물이 미국과 유럽행 항로로 대량 집결하면서, 싱가포르·타이베이·홍콩·인천 환적 허브가 포화 상태에 가까워지고 있다.”고 전언,

- 즉, “항공화물의 전통적 성수기이지만, 올해는 특히 동남아에서 폭발하는 수요 강도가 다르다며, . AI 및 첨단 제조업 연계 화물이 환적 허브들을 사실상 만석에 가깝게 만들고 있다”고 함.

- 이에 따라 포워더들은 고객들에게 지연을 피하기 위해 출하를 최소 1~2주 앞서 예약할 것을 권고하고 있으며, 긴급 화물의 경우 출발지나 환적 허브를 유연하게 조정하는 것이 혼란을 줄이는 방법으로 제시.

- 해상운송 시장은 대조적으로 약세, 주요 항로 전반에서 수요 부진이 이어지자 선사들은 골든위크 기간 운항 축소를 단행하며 운임 안정을 꾀하고 있음.

- 선박 공급은 수요를 상회하고 있으며, 운항사들의 영업이익률은 지난 18개월 사이 최저 수준 하락, 이에 따라 선사들은 공급 조절과 운임 방어 압력에 직면. 컨테이너 시장 관계자들은 10월 하반기 Blank Sailing 증가 가능성을 예고하며, 아시아-미국행 화물은 유연한 경로 선택과 조기 예약을, 아시아-유럽행 화물은 4분기까지 운임 변동성 지속에 대비할 것을 당부.

3) 중국, 미국관세 피해 신흥국으로 à 저가수출 폭주 속 최대 흑자 전망

- 중국이 미국 고율 관세를 피해 저가 제품 수출을 크게 늘리며, 올해 사상 최대(1.2조 달러)의 무역흑자 기록 전망

- 올해 1∼8월 중국 무역흑자 규모는 7,858억 달러로 작년 동월(6,126억 달러) 대비 28.2% 급증

- 중국이 미국 관세를 피해 인도 · 아프리카 · 동남아시아 등 신흥시장으로의 수출을 대폭 확대하고 있어, 관련국 들은 반덤핑 조사 압박을 받고 있는 상황 (인도, 최근 중국 등 상품 덤핑에 대한 조사 신청 50건 접수)

- Bloomberg는 중국의 공세적 수출 전략 타깃이 된 국가들이 적극적인 조치에 나설 가능성은 낮게 평가

- "이미 미국과의 관세 협상에 휘말린 국가들은 세계 2위 경제 대국(중국)과의 무역전쟁을 꺼리고 있다" 고 전언.

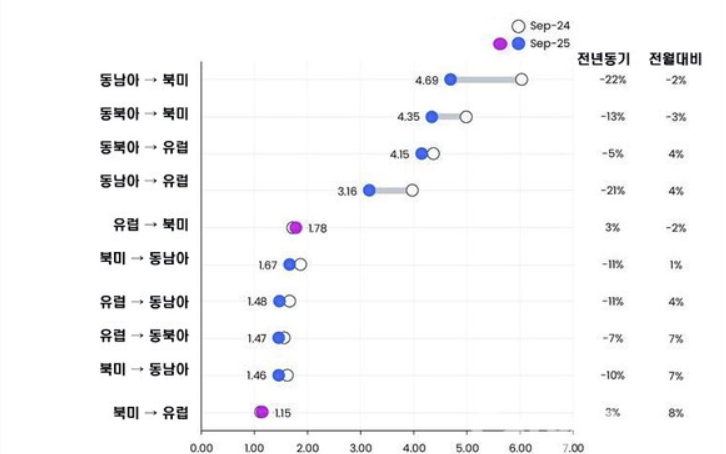

4) 글로벌 평균 항공운임은 $2.54로 4% 하락

- 지난 9월 기준 세계 항공화물 평균 운임은 2.54달러/kg로 전년동기 대비 4% 낮은 수준을 유지. 지난 5월 이후 전년동기 대비 3~4% 하락세를 5개월 연속 유지.

- 항공화물에 대한 수요와 공급은 전년동기 대비 3%가 각각 증가, 9월 항공화물 수요 2024년 월평균 = 100)는 105'로 비교적 강세를 유지. 항공화물 수요(2024년 월평균 =100) 역시 105'로 나타났는데, 이에 따른 항공화물에 대한 평균 적재율은 59%로 전년동기 대 비 1% 하락.

- 특히 미국의 건당 800달러 이하 소액 물품에 대한 목록통관 금지와 관세 부과로 전자상거 래를 중심으로 미국노선에 대한 항공화물 수요가 크게 감소, 대신 유럽노선의 전자상 거래 수요는 증가.

- 태평양노선과 대서양노선 모두 운임도 전월대비 2~3% 하락. .

- 주요 노선별 운임은 동남아 - 북미노선의 운임은 498달러/kg으로 전년동기 대비 22%가 하락한 수준인데, 동남아 - 북미노선 운임도 435달러kg로 전년동기 대비 10%, 동북아 - 유럽노선도 4.15달러/kg로 9%가 각각 떨어진 수준을 유지.

- 또 지난 3분기 기준 포워더와 화주 간 항공운임 계약 관계는 6개월 이하 단기계약 비중이 전년대비 증가함. 신규 항공운임 계약을 기준으로 1년 이상 계약기간이 2%, 12개월이 44%, 6개월이 23%, 3개월은 20%를 각각 차지. 또 3분기 기준 포워더와 항공사 간 1개월 이하 현물운임 계약비중은 48%.

5) Airlines Movement

- 페덱스(FX),: HAN – ICN – CAN 주1회 화물노선 신설

-> HAN발 전자제품 & 섬유 등 고수요 분야를 중심으로 수출 지원 예정

- DHL Express(D0) : HAN발 HKG 경유 화물노선 주6회 운항 (B777, A330)

- 아시아나항공(OZ) : 9월 5일부터 12월 31일까지 ICN – FRA 여객노선 주5회 운항 재개 (A380)

-> ‘26년 1월 15일부터 3월 28일까지 ICN–BKK 여객노선 주11 → 14회 증편 (A321N, A359)

- 마틴에어카고(MP) : 10월 28일부 ICN – HKG – AMS 화물노선 주1회, ICN – AMS 직항 주2회 운항 (B744)

Share this article :

top