세상을 움직이는 물류의 힘!

바로 엑스트란스의 힘입니다.

2024년 22주차 자료 전달드립니다

항공화물 General

1) 항구 혼잡 심화로 SEA & AIR 서비스 불가로 중동 환적 거점서 리드 타임 늘어

- 해상 공급망 혼란은 결국 항공화물 공급 부족 초래 예상

- 홍해 사태 영향으로 주요 항구들의 혼잡도가 늘면서 그동안 상대적으로 긴급을 요하는 화물을 위해 활성화되었던 아시아-유럽 구간 환적을 통한

SEA &AIR가 사실상 실행되지 못하고 있다는 지적이 나옴.

- SEA & AIR 전문 시장 플레이어들은 “싱가포르나 포트 클랑을 경유해 움직이던 SEA & AIR 서비스가 해당 항구들의 혼잡이 늘면서 사실상 이를

이용할 수 없다”고 지적하면서 “특히 일부 항구에서는 선박 도착과 정박까지 최대 7일 이상이 소요되고 있어 상대적으로 신속한 서비스를 원하는

화주들의 요구를 충족시키지 못하고 있다”고 밝힘.

- 더욱이 두바이의 경우는 공항 화물게이트 혼잡이 크게 증가하면서, 항만과 함께 환적지로서 매력이 떨어지고 있다는 지적.

- 한 관계자는 “일단 그동안 두바이의 Jebel Ali항구는 희망봉 우회에 따른 추가 운송시간을 크게 줄일 수 있다는 점에서 화주들의 선호도가 매우 높았지만

- 홍해서 항로를 바꾸려는 선박들이 늘면서 교통량이 급등, 매우 혼잡해지고 있다고 함. 이는 같은 역할을 해온 Dammam도 비슷한 상황 ”이라고 지적.

- 이에 따라 시장 전문가들은 홍해 사태 여파가 점점 심화되고 있어, 아시아- 유럽 구간의 항공화물 시장이 조만간 더 큰 공급 부족을 겪을 수도

있다고 보고 있음. 특히 통상적으로 경험해온 “해상 공급망 위기 >> SEA & AIR 활성화 >> 항공화물 공급 부족”의 순차적인 여파가 현실화될

가능성에 무게를 두고 있음.

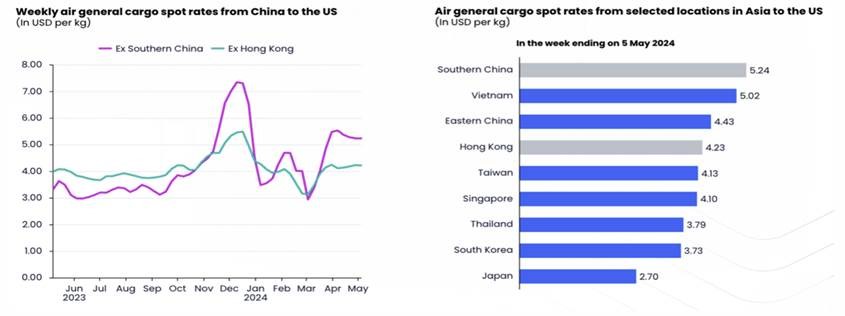

2) 아시아발 미주행 항공화물 운임 시황

- 주요 전자상거래 발원지인 중국남부 (Southern China)와 홍콩(Hong Kong)의 항공 화물운임은 작년 성수기 말부터 지속적 상승세.

- 5월 첫째주 동안 일반 화물 기준 현물운임은 중국 남부에서 미국행 $5.24/kg을 기록함.

- 홍콩에서 미국행 $4.23/kg으로집계됨. 두차선 모두 여전히 2019년 같은 기간에 비해 약 85% 더높음.

- 이는 전자상거래 급증 이전에 보였던 두 지역간의 전통적인 운임 수준이 아님. 화주가 다른 이용가능한 노선을 찾으면서 이러한 추이는

인근 항공화물 허브까지 확장됨.

- 예를들어, 5월 첫째주 베트남에서 미국으로 향하는 일반화물 현물운임은 kg당 $5.02로 2019년 같은기간에 비해 거의 60% 급등함.

- 5월 첫째주 일반화물 출발운임(현물)은kg당 중국동부(Eastern China)는 $4.43, 대만은 $4.12, 싱가포르 $4.10, 태국 $4.13, 한국 $3.73,

일본 $2.70 미국행 운임을 기록함.

- 앞으로 있을 잠재적으로 '강한성수기’ 에 대비하여 스페이스 확보 전략이 매우 중요함

3) 중국발 항공화물 수요는 지속 상승 기조

- 올들어 20번째 주(5월 13일~19일) 기준 세계 평균 항공화물 운임은 2.48달러/kg으로 전주 대비 약간 상승. 전년동기 대비로는 2% 상승.

- 팬데믹 이전인 2019년 5월 평균 운 임에 비해선 40%가 높은 셈. 항공화물 수요도 전년동기 대비 9% 증가.

- 아태지역이 15%, 중동 동남아가 16% 증가하면서 전반적인 상승세를 주도.

- 특히 두바이(DXB)에서 유럽노선에 대한 항공화물 수요가 148%나 급등. 이에따라 중 동 동남아에서 유럽노선 항공화물 수요는 전년동기 대비 31% 증가.

- 두바이발 항공화물의 급증은 홍해사태로 중동 경유 해운•항공 복합운송(Sea & Air) 물동량이 급격히 증가했기 때문. 이 밖에도 스리랑카발도 57%,

방글라데시도 28%가 각각 증가.

- 이같은 수요 급증으로 방글라데시에서 유럽행 운임은 4.66달러/kg. 전년동기 대비로는 136%나 오른 셈. 인도에서 유럽향 운임도 372달러/kg으로

- 전년동기 대비 163%나 상승.

- 아태지역발 항공화물 수요도 전년동기 대비 15% 증가. 이에따라 운임도 10%가 올랐 특히 홍콩(HKG)과 중국에서 유럽노선 운임은 지난 14주와 18주

사이에 각각 23%외 47%가 상승.

- 올들어 19번째 주와 20번째 주 항공화물 수요는 19%와 10%가 각각 증가. 홍콩과 중국에서 유럽노선에 대한 전년동기 대비 항공화물 수요는 31% 증가.

- 최근 한 달 사이에 중국에서 유럽노선 운임은 22~31%나 올랐는데, 홍콩발 운임도 3~23% 상승. 특히 베트남발 유럽노선 운임은 4달러/kg로 꾸준히

강세를 유지하고 있다 이는 전년동기 대비 120%나 높은 수준

4) 미·중 갈등에 인도·아세안으로 공급망 중심축 이동할 것으로 전망.

- 미국과 중국의 갈등 심화로 글로벌 공급망 무게추가 인도와 아세안 지역으로 이동하고 있음.

- 최근PwC가 아시아, 유럽, 북미지역 기업의 고위임원 150명을 대상으로 실시한 설문조사에서 향후 10년간 인도의 글로벌 기업 공급망 순위는

4위에서 3위로 올라설 것으로 집계됨.

- 아세안도 한단계 상승한 5위를 차지할 것으로 보임, 반면에 독일은 한계단 하락한 4위로, 일본은 6위로 밀려날 것으로 나타남.

- 아세안은 전자 제조부문의 재조정에서, 인도는 전자제조, 제약 및 의료장비 부문에서 혜택을 볼 것으로 예상됨.

- 글로벌 기업들은 공급망 복원을 강화하는 동시에 지나친 단일시장 의존을 낮추는 등 공급망을 재조정하고 있지만, 미국과 중국은 가까운 미래에도

여전히 상위공급망으로 남아 있을 전망임.

- PwC는 아세안 10개 회원국과 인도가 대체 공급망으로 주목받을 것으로 전망함. 남아시아와 아세안은 높은 인구밀도와 경제성장률로 다국적기업에

다양한 수익성 기회를 제공할 수 있기 때문임.

- PwC는 비즈니스 리더들이 공급망 재조정과 외부 압력에 대한 기업의 회복력 강화 필요성을 우선 순위에 두고 있다고 평가함

5) 항공사/GSA Event update

(1) 국토부, 국제선 30개 노선 운수권 배분

주목되는 점은 부산을 거점으로 취항 준비중인 시리우스 항공이 전체 운수권 중 10개 화물노선을 받음.

한/카자흐스탄 화물노선에는 아시아나 주 8회, 에어인천 주 6회, 시리우스 주 6회의 운항이 가능. 인천/울란바토르은 에어인천이 주 2회 운항권 확보.

이외 시리우스 항공은 한/폴란드 주 2회, 한/카타르 주 4회, 한/이스탄불, 앙카라 주2회 확보.

국제노선 다양화를 통한 LCC 경쟁력 확보에 심혈을 기울인 것으로 분석. 그동안 동북아, 동남아 위주로 운항했던 국내 LCC가 인도, 우즈베키스탄, 카자흐스탄, 키르기즈스탄 등

서남아시아와 중앙아시아에도 취항할 수 있게 됨. 인천-알마티(이스타 주 2회), 한-우즈벡(제주 주3회, 티웨이), 서울/뉴델리,뭄바이(티웨이 주3회)등으로 중거리 노선 확대도 이루어질 전망.

(2) 세인, 테무 하루 B777화물기 88대 수요

중국 전자상거래 업체인 셰인과 테무가 전세계적으로 운송하는 항공화물은 하루 9000톤에 달함. 이는 B777F 88대에 달하는 수송능력으로 전자상거래 업체들의 물동량

흡수력으로 항공화물 운임이 전반적인 상승 기조를 유지하고 있는 것으로 분석. 애플이 하루 약 1000톤의 항공화물을 운송하는 것과 비교할 때 막대한 물동량.

작년 기준 테무의 매출은 241% 증가. 세인 역시 영업이익이 3배 증가. 이 같은 영업이익을 바탕으로 전자상거래 업체들은 항공운송을 통한 글로벌 물류 영토를 점차 강화 중.

현재 세인의 경우 전세계 장거리 화물 전세편의 약 30% 이상을 사용 중. 지난 4월 기준 중국발 항공화물 운임은 14% 인상.

(3) 티웨이항공(TW) 파리 취항 스케줄 발표

ICNCDG 3W(D136) TW401 1135/1810, CDGICN TW402 2030/1515+1 A332, 7/1부 * 확정스케쥴은 아님.

Share this article :

top