세상을 움직이는 물류의 힘!

바로 엑스트란스의 힘입니다.

2024년 9주차 자료 전달드립니다

Air Cargo General

1) 아시아나항공 화물 인수전에 물류대기업+LCC '연합군' 구성될까?

- 대한항공이 추진하는 아시아나항공 화물사업 부문 매각을 위한 예비 입찰이 오는 28일 마감. 국내 저비용항공사(LCC) 5곳이 인수를 검토 중인 가운데,

-

LCC와 손잡고 인수전에 뛰어들 물류 대기업이 나올지 관심이 쏠리는 중.

- 아시아나항공 화물사업부 매각 주관사인 UBS는 잠재 인수 후보들을 대상으로 티저레터(투자설명서)를 발송. 인수 희망 업체는 28일 오후 2시까지

-

자금 조달 계획서와 사업계획서를 포함한 입찰제안서를 제출.

- 아시아나항공 화물사업부는 자체 보유한 화물기 8대와 리스(임대) 화물기 3대 등 총 11대를 보유. 지난해 매출은 1조6071억원, 국내외 화물 수송량은

-

연평균 75만t 정도. 국적 항공사 중 대한항공에 이어 두 번째로 큰 규모. 항공업계는 아시아나항공 화물사업본부 매각가를 5000억∼7000억원

(부채 1조원 별도)으로 예상.

- 하지만 항공업계는 협상 과정에서 매각가가 더 떨어질 수 있다고 봄. 아시아나항공이 대형 여객기에 화물을 탑재해 운송해온 '벨리카고' 수익이

-

그동안 화물사업부에 반영됐던 터라, 인수후엔 실 매출에서 빠짐. 또 상당수 기체가 25년이 넘어 노후화. 더구나 인수시 1조원 규모의 화물사업부

부채도 떠안아야 하는 만큼 예비 인수자들은 최대한 인수가격을 낮출 것으로 보임.

- 이번 인수전의 핵심은 자금력. 최대 1조원 이상의 자금이 투입되는 대형 인수 건이기 때문. 사모펀드가 대주주로 있는 이스타항공과 에어프레미아가

-

유리하다는 평가가 나오는 이유. 이스타항공은 VIG파트너스가, 에어프레미아는 JC파트너스가 대주주. 이들 사모펀드는 1조원 이상의 자금을 운용.

반면, 제주항공은 신중한 모습. 보유 현금이 3000억원에 불과하고 이미 자체 화물 사업을 진행하고 있기 때문. 인수를 위해선 모기업인 애경의 참여가

불가피한 만큼 인수 참여는 더욱 신중하게 결정할 계획.

- 에어로케이는 아시아나항공 인수전의 다크호스로 떠오름. 지난 22일 아시아나항공 화물사업본부 인수에 참여한다고 공식 선언. 에어로케이의 대주주는

-

대명화학그룹. 다양한 패션 브랜드와 로젠택배를 보유하고 있는 만큼 물류 시너지를 기대하고 인수전에 참여한다는 입장. 자금 동원력도 탄탄한 것으로

알려짐. 이밖에 국내 유일 화물 항공사 에어인천도 이번 인수전에 나설 예정이지만 자금력 면에서 가장 약체라는 평가임.

- LCC들은 전략적 투자자(SI)로 물류 대기업을 유치하기 위해 물밑 경쟁 중. 물류 기업이 SI로 참여하면 인수 후에도 화물 물량을 안정적으로 확보할 수 있고,

-

장기적으로는 LCC 대주주인 사모펀드들이 해당 SI에 지분을 넘기고 엑시트(투자금 회수)할 수도 있음. 어제일 먼저 거론되는 곳은 LX그룹. 상사인

LX인터내셔널, 물류기업 LX판토스 등을 보유. 범LG가의 물량을 바탕으로 물류 사업에서 시너지를 낼 수 있다는 평가. HMM 인수전에서 고배를 마신

동원그룹 이름도 오르내임. 동원그룹은 2017년 동부익스프레스를 인수하며 화물 운송과 국제 물류 등 사업 기반을 갖춘 상태. 투자 업계 관계자는

"대기업은 물론 중견기업 등 다수의 SI가 관심을 갖고 매각 주관사에 문의하고 있다”고 설명.

- 그러나 일각에선 매물의 가치를 평가할 만한 정보가 부족하다는 불만. UBS를 통해 배포된 투자설명서(IM)에 화물사업부의 손익은 물론 자산·부채 정보도

-

전혀 제공되지 않았다고 함. 항공업계 관계자는 "대한항공이 적극적으로 매각 사업부에 대한 정보 등을 공개해야 정상적으로 절차가 진행될 것"이라고

말함. 대한항공은 오는 10월 전에 매수 최종후보 선정을 마칠 계획. 인수자가 선정되면 유럽연합(EU) 경쟁 당국 승인을 거쳐 분리 매각이 마무리.

2) 아시아-유럽 SEA & AIR 허브 공항 실적 증가

- 홍해사태로 인한 많은 영향중 하나는 해상운임 상승 및 지연의 여파로 아시아발 유럽행 SEA & AIR 서비스가 늘어날 것이라는 점. 최근 글로벌 항공화물 시장 분석 업체인 WordlACD의 주간 보고서에는 이 같은 시장의 전망이 그대로 드러냄.

- 지난 1월 18일 기준 7주차 글로벌 항공화물 시장 동향을 보면, 최근 몇 주 동안 두바이, 콜롬보, 방콕과 같은 SEA & AIR 환적 거점공항들의 항공화물 수요가 넘쳐나는 것을 확인할 수 있는데, WorldACD측은 “올들어 첫 7주간 이들 공항들의 실적을 보면, 지난해 1월 첫 7주간 실적보다 50% 이상 대폭 증가세를 시현, 두바이- 유럽 구간 수송량은 71%, 콜롬보-유럽은 61%, 그리고 방콕-유럽은 58%가 증가한 것으로 집게되고 있다”고 함.

- 이는 싱가포르- 유럽 구간이나 도하-유럽 구간이 전년동기비 3%~10% 전후의 실적 증가세를 보인 것과 확실히 차별화되는 부분이라는 것.

- 특히 중국의 춘절 기간이 포함된 7주차(2월 12일~18일)만 봐도 이들 3대 공항의 유럽행 톤수는 크게 증가했는데, 두바이-유럽이 7주차 기준

161%(최근 3주간으론 89% 증가)로 3배 이상 늘었고, 또한 방콕-유럽은 7주차만 볼 때 112% 증가(3주간 기준으로 77%)했고, 콜롬버-유럽은

112%(3주간 기준으론 77% 증가)이나 증가한 것으로 나타남.

- 한편 7주차 기준 글로벌 항공화물 수요톤수는 전주 대비 10% 이상 하락하면서 중국 춘절 이후 일반적인 수요 감소와 운임 하락 추세를 그대로 반영.

3) 이커머스 성장에 덩달아 웃은 물류의 봄날 계속될까

- 중국 이커머스 플랫폼의 초저가 공세가 이어지는 중. 알리익스프레스, 테무 등 중국 플랫폼은 '물량'을 앞세워 국내 이커머스 시장을 빠르게 잠식. 도매사이트인 1688닷컴의 한국 상륙도 임박

- 현재 한국 이커머스 물류 서비스 1위 기업은 단연 CJ대한통운. CJ대한통운은 지난 7일 공시를 통해 2023년 매출 11조7679억원, 영업이익 4802억원을 기록하며 영업이익이 전년 대비 16.6% 증가.

- CJ대한통운이 네이버, 알리익스프레스(알리) 등 국경을 막론하고 이커머스의 물류 강자로 자리 잡게 된 비결은 풀필먼트(fulfillment) 서비스. 택배사에서 전 과정을 통합해 관리하기 때문에 판매자는 물류 관리 부담이 줄어듬.

- 여기에 더해 2021년 로봇·AI빅데이터 등을 통해 혁신 기술기업으로 거듭나겠다는 미래 비전을 발표. 이후 물류 기술 개발을 담당하는 'TES물류기술연구소' 규모를 2배 이상 키우는 등 물류 자동화 투자를 확대 중 .

- CJ대한통운이 물류업체로서 이커머스와 파트너십을 공고히 했다면 쿠팡은 반대로 이커머스 업체로서 자체 물류에 투자한 경우. 쿠팡은 지난해 수십년간 부동의 1위였던 이마트를 넘어서며 명실공히 유통 최강자로 등극. 여기에는 십수년 동안 '밑 빠진 독에 물 붓기'라는 말을 들어가면서도 물류에 지속적인 투자를 아끼지 않은 것이 큰 역할을 함.

- 쿠팡의 핵심 경쟁력은 '로켓배송' . 창립 후 6조2000억원가량을 전국 물류망 구축에 투자해 이른바 '쿠세권'(로켓배송 가능 지역)을 대대적으로 확대하는 데 총력을 기울임. 2022년에는 아시아권 최대 풀필먼트센터 중 하나인 대구FC 건립을 위해 3200억원 이상을 투자, AI, 물류 로봇 등이 접목된 최첨단 물류 기술과 설비를 대거 투입.

- 투자와 노력의 결실이 가시화되어 지난해 1~3분기 누적 매출은 23조1767억원, 영업이익은 4448억원. 특히 3분기 매출만 8조원을 돌파하면서 업계에서는 연 매출 30조원을 넘길 것으로 봄.

- 이러는 가운데 국제 물류와 판매 플랫폼 모두 접수한 큐텐, 알리 대항마 될까?

- 큐텐은 지난 13일 위시 인수로 단번에 한국계 기업 최초의 글로벌 마켓플레이스로 발돋움. 위시는 전 세계 200여개 국가에서 33개 언어로 서비스 중인 미국의 글로벌 이커머스 플랫폼. 큐텐은 이번 인수를 통해 그동안 상대적으로 열세였던 북미와 유럽 지역의 고객은 물론 남미, 아프리카를 포함한 광범위한 글로벌 공급망을 확보.

- 무엇보다 주목해야 할 점은 위시가 44개국에 통합 물류 솔루션 바탕의 4자물류(4PL)를, 16개국에는 3자물류(3PL) 서비스를 제공하고 있다는 점.

- 큐텐은 기존에도 물류 자회사인 큐익스프레스를 통해 국내 판매자에게 해외 판매 기반을 제공.. 계열사인 티몬과 위메프, 인터파크커머스 등에 입점한 판매자는 큐익스프레스의 풀필먼트 서비스인 'Qx프라임'을 이용해 국내외 통합배송과 글로벌 물류 인프라를 활용 가능. 지난해 경기도 이천에 연면적 3만3000㎡ 규모의 물류센터 'QDPC이천'(Qxpress Digital Partner Center)을 열고 서비스를 확장.

- 업계에서는 큐텐이 위시 인수로 글로벌 공급망을 확보한 만큼 세계적인 크로스보더 업체인 아마존, 알리 등에 도전장을 내밀 정도로 성장할지 주목.

4) 설연휴 이후 중국발 항공운임 주춤

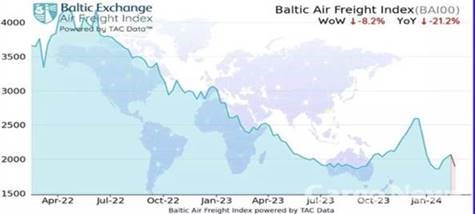

- 항공화물 운임이 아시아권 연휴이후 하락세를 나타냄. 지난 2월 19일 기준 세계 평균 항공화물 운임은 전주대비2% 떨어지. 전년동기 대비로 는 21.2%가 하락. 특히 홍콩(HKG)발 운임은 전주대비 -13% 기록.

- TAC가 집계해 발표하는 '발틱항공운임지수(BA)'에 따르면 상하이(PVG)발 항공운임도 전주 대비5% 하락. 전년동기 대비로도 5.4%가 하락한 셈. 이같은 항공운임 하락은 중국이 연휴이후 제조업체들이 아직 본격적인 생산을 하지 않고 있기 때문으로 분석.

- 홍해사태로 두바이(DXB)와 방콕(BKK)에 대한 항공화물 수요는 증가 중. 인도도 유럽 과 미국에 대한 항공화물 수요가 증가하고 있는 것으로 분석. 해상 공급망 혼란으로 항공시장으로 대체 수요가 몰리고 있기 때문.

- 한편 프랑크푸르트(FRA)발 운임은 전주대비7%가 상승. 이는 프랑크푸르트에서 중국 과 동남아에 대한 수요가 증가했기 때문. 전년동기 대비로는 여전히 39.7% 낮은 수준임. 런던(LHR)발 항공운임도 전주대비 6.9% 떨어짐. 전년동기 대비로는 여전히 51.3% 가 낮은 상태.

- 하지만 미국 시카고(ORD)발 운임은4% 상승. 아시아에 대한 항공화물 수요가 증가 했기 때문. 전년동기 대비 시카고발 운임은 여전히 31.3%가 낮은 상태.

5) 항공사/GSA Event update

(1) 대한항공, 티웨이에 최신형 A350 임대 방안 검토

대항항공은 최근 아시아나 A350-900 항공기에 대한 임대 의사를 최근 티웨이항공에 전달한 것으로 알려짐.

아시아나는 A350-900 15대를 장기 리스해 운영 중으로, 대한항공이 합병 후 이 중 3대를 티웨이항공에 임대한다는 계획.

앞서 대한항공은 티웨이항공에 A330-200 항공기 5대를 지원, 현재 티웨이항공이 보유한 대형 항공기는 3대이며 올해 2대를 더 들여올 예정.

TW는 4월 자그레브, 6월 파리, 8월 로마, 9월 바르셀로나, 밴쿠버, 10월 독일 프랑크푸르트에 차례로 취항할 계획.

여기에 아시아나의 A350-900 3대까지 더하면 티웨이항공은 경쟁력은 더 향상될 것으로 예상.

(2) 아메리칸항공(AA) JFK-HND노선 매일 직항 운항

6월 28일부터 이 노선을 매일 운항.

JFKHND 1125/1430+1, HNDJFK 1630/1635 B772, 6/8일부

(3) 말레이시아 항공(MH), 쿠알라룸푸르-인천 주 12회 증편

추가 5편(D14567) ICNKUL MH039 0010/0545, KULICN D34567 1450/2230, 4/25일부 A333

(4) 가루다 인도네시아(GA), 인천-자카르타/발리 노선을 총 주 12회 증편

ICNCGK 4Wà5W(D23567) GA879 1035/1540, CGKICN D(12467) 2315/0830+1,A333

ICNDPS 4Wà7W GA871 1125/1720, DPSICN GA870 0115/0915, A333

(5) 인도 정부, 3년 간 외국적 화물항공사 화물기 운항 자유화

최근 인도내 모든 국제공항을 외국적 화물항공사가 운항할 수 있도록 항공정책 자유화 선언. 3년 간 유지.

Share this article :

top